Stocks slipped this morning following yesterday’s major blast higher. The Dow, S&P, and Nasdaq Composite all traded slightly lower through noon. Shortly after the market opened, equities ticked higher on Ukraine peace optimism.

Reuters reported today that the Ukraine foreign minister said his country is “ready to continue diplomatic efforts to stop Russian aggression.”

Roughly an hour later, though, US officials told Reuters that there is “still a very big gap between positions in the Ukraine peace-talks.”

Stocks fell again while gold climbed. The “icing on the (bearish) cake” could be coming later this afternoon, likely in the form of a comment from Russia’s foreign minister suggesting that talks have gone poorly – something he’s done several times now.

But the bigger news of the day has to do with the Fed’s rate hike, and more specifically, the number of hikes that have yet to come.

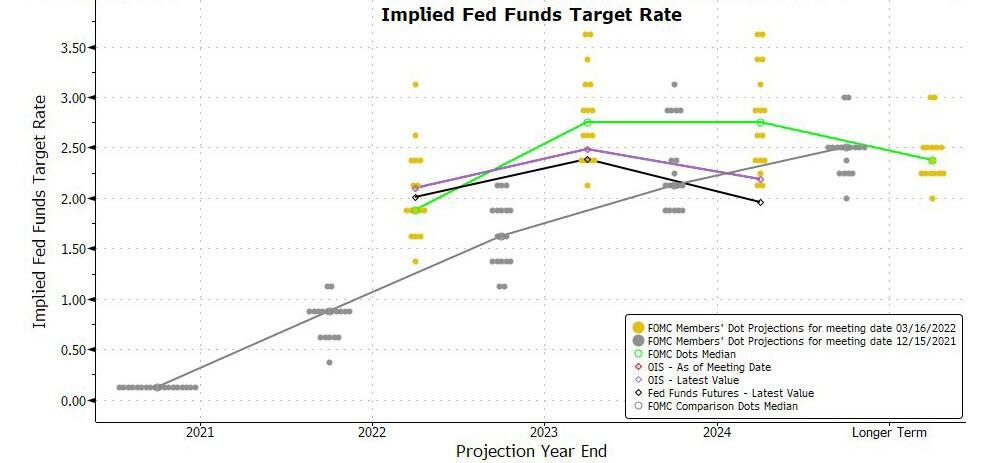

The FOMC’s “dots,” as charted above, jumped so high that the Fed more or less confirmed the market’s fears. Six additional hikes are now expected by the Fed in 2022, which would result in rate increases following every remaining FOMC meeting this year.

And while that may seem like a bearish impulse, to traders yesterday, it ultimately skewed bullish. The Fed only raised rates by 25 basis points (bps), matching the consensus estimate. A more hawkish hike (50 bps) would have caused stocks to drop.

What really drove share prices higher, though, were plunging yields after the Fed said it expected 6 more hikes this year. The US Treasury 10-year/5-year spread (5s10s) even temporarily inverted, doing so for the first time since May 2019.

The more-watched US Treasury 10-year/2-year spread (2s10s) has yet to invert, however it seems like only a matter of time before it follows suit. It should be noted that every time a hiking cycle inverts the 2s10s, a recession has followed within 1 to 3 years afterward.

Fed rate hikes in late 2018 caused the 2s10s to invert in 2019. The Covid slowdown arrived less than a year later.

Deutsche Bank’s Jim Reid wrote in a note today about the chances of a 2s10s inversion in the coming months.

“There is a decent likelihood that the curve inverts relatively early on. 2s10s peaked at +157.6 bps last March and traded as low as +21.9 bps last week before settling at around +30 bps as we go to print.”

5s10s inversions have historically preceded 2s10s inversions by several weeks. If that trend holds, the 2s10s will flip negative by the end of April.

That’s ironically a major bullish signal, because it suggests that the Fed will ramp up quantitative easing (QE) again while lowering rates in response to a nearly guaranteed recession.

This could have a disastrous effect on inflation long-term, which would cut deeply into the market’s real returns over time. Stocks would continue climbing in this scenario in terms of nominal gains, but no real money would be made as inflation outpaces equities.

That’s a worst-case scenario, of course. But based on Treasury trading activity, it seems to be both the most likely outcome and what investors expect will happen.

For everyone’s sake, I hope they’re ultimately proven wrong. The truth is that they’re probably right, however, and that’s what should have long-term, “buy and holders” feeling nervous about the next few years.

{kind=link}