The market’s rising again this morning, led by a tech recovery and better than expected economic data. The Dow, S&P, and Nasdaq Composite are up 0.50%, 0.90%, and 1.40%, respectively, as of noon.

And, unsurprisingly, Big Tech is enjoying some of the day’s biggest gains. Apple (NASDAQ: AAPL) and Google-parent Alphabet (NASDAQ: GOOG) are seeing lifts of over 2% while Netflix (NASDAQ: NFLX) and Facebook (NASDAQ: FB) climb 3% higher as well.

Even Tesla (NASDAQ: TSLA), which plummeted immediately after peaking on September 1st, is heading back toward its all-time high. The stock is currently up 6%.

Investors were pleased to hear that China’s retail sales may nearly be fully recovered. Beijing reported a retail sales increase of 0.5% in August, marking the first increase in that statistic for 2020.

“[China’s] on track to return to its pre-virus growth rate before the end of the year,” explained Julian Evans-Pritchard, senior China economist at Capital Economics.

“Retail sales surpassed 2019 levels for the first time since the COVID-19 outbreak, while investment and output growth continued to strengthen.”

Stateside, the Empire State Manufacturing (ESM) index blew away analyst estimates. Polled economists expected a reading of 7. The ESM clocked-in at 17 for September. In August, the index reported a disappointing 3.7 measurement by comparison.

But perhaps the biggest bullish influence today was a continued return to normalcy in the business world. CNBC’s Jim Cramer said this morning that the Trump administration will approve the Oracle-TikTok deal. Nvidia’s buying Arm Holding from SoftBank for roughly $40 billion, too.

In other words, corporations are moving forward with aggressive acquisitions in spite of a Covid-stricken economy. Increased capital expenditures (CapEx), or business investments, have historically been seen as a good sign for future growth.

The recent moves by America’s top companies should be viewed with the same lens.

“Regardless of the situation, regardless of the sector, big commitments and big mergers tend to show confidence, and we would take those as positive signs,” said LPL Financial analyst Jeff Buchbinder.

Buchbinder’s firm raised its year-end target for the S&P 500 to 3,450-3,500 on Monday, which would put the index below its record high from early September.

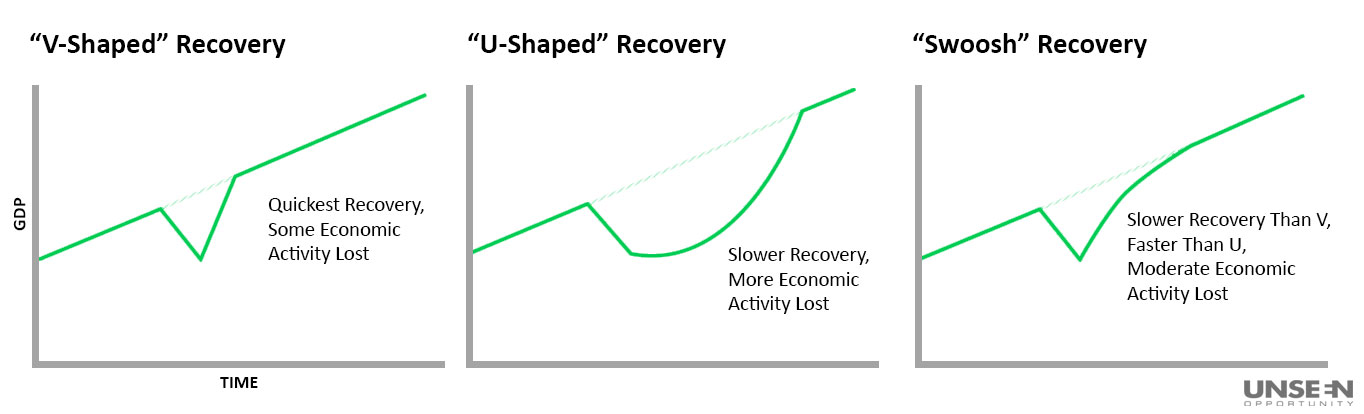

It’s not an overly bullish prediction considering that the S&P 500 would only need to rise roughly 1% to finish in that range. But, in this case, simply avoiding a sell-off could be a major win for the market. Most economists believe that the U.S. isn’t going to complete a “V-shaped” recovery.

Instead, they claim a “swoosh” is more likely.

Thus far, the U.S. is leaning towards “V,” but it has yet to finish a full recovery of that manner. A “tailing off” period is expected from here – something that could spell doom for bulls near the all-time highs.

The question is whether the market has already priced-in an assumed “V-shaped” recovery or not. If investors are prepared to remain realistic about managing their expectations, LPL Financial’s forecast should prove accurate.

But, if the market ends up demanding “V-shaped or bust,” a correction could be in order. And with a critical presidential election approaching, investors will be tuned-in to the economy and its ongoing recovery.

Regardless of who wins come November.

{kind=link}