The World Health Organization (WHO) declared the Wuhan coronavirus a global health emergency yesterday. 9,776 people are infected. 187 have recovered, opposite the 213 who have died.

But instead of finishing out yesterday’s trading session on a low note, stocks closed higher. The WHO’s “emergency” designation released financial aid for affected areas, as well as additional manpower. To bulls, it was confirmation that the coronavirus was finally being taken seriously.

This morning, however, sentiment has shifted once again.

The market opened lower today despite a massive earnings beat from Amazon (NASDAQ: AMZN), which saw major Q4 rewards for its Q3 investments in one-day shipping. AMZN shares started the day with a whopping 9% gain as a result.

And though equities may be trading at bargain prices (relative to the highs of last week), some analysts think the market could fall further. Buying back in right now, they say, could be a “huge mistake.”

Kevin Smith, chief investment officer at Crescat Capital, told clients this week that “the bear case for U.S. stocks has never been stronger,” and that the current situation needs to be viewed with much more scrutiny by investors.

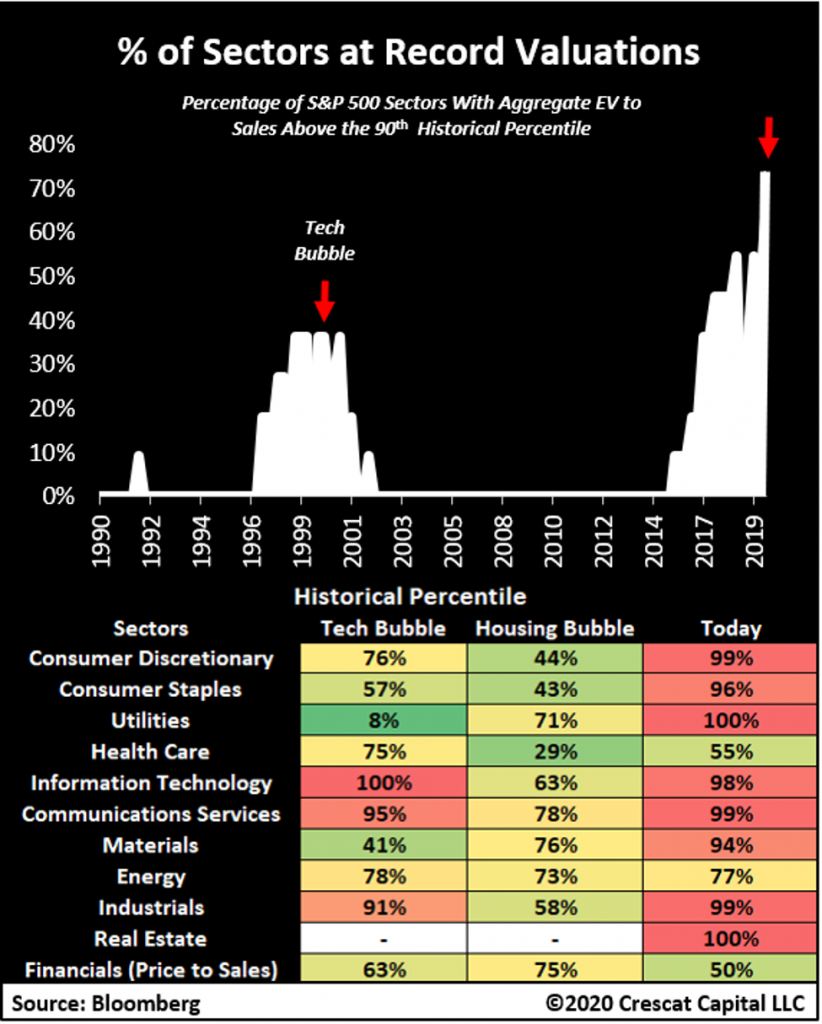

“We certainly did not predict the Coronavirus, but it may prove to be the catalyst to tip this market that is trading at truly historic valuation levels after a record long U.S. economic expansion,” Smith wrote in a note, reflecting his firm’s belief that bulls continue to overvalue stocks.

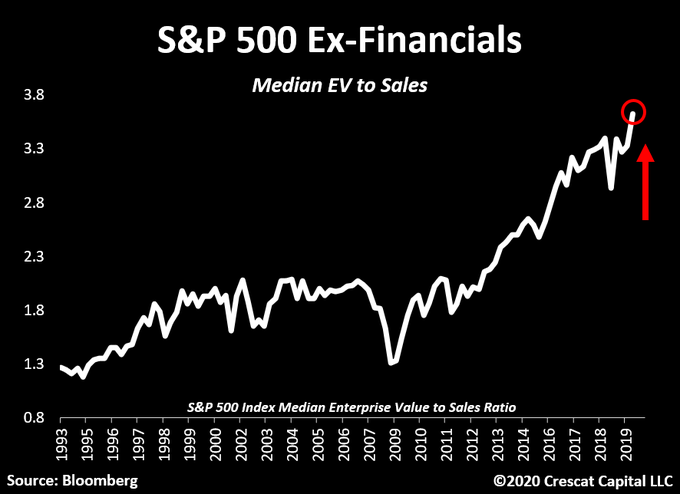

“Median [Enterprise Value]-to-sales for the S&P 500, based on our work recently reached an insane, euphoric level of 3.6 times, two times than the tech bubble peak.”

Enterprise value (EV)-to-sales – the metric upon which Smith bases his viewpoint – is a financial ratio that compares the total market value of a business to its sales. EV differs from stock price in that it includes claims from creditors and shareholders in the company’s complete valuation. For that reason, many analysts – Smith included – prefer EV-to-sales over price-to-sales when determining a stock’s “true” value.

To further illustrate his point, Smith released the following chart, comparing the current market to how it looked pre and post-tech bubble in terms of heightened EV-to-sales.

Incidentally, EV-to-sales ratios weren’t nearly as “overweight” during the 2008 financial crisis as they are now. Of course, the cause of the crisis was subprime mortgages – not overvalued companies – but it could be argued that the ensuing crash would’ve been worse had stocks resembled their current valuations.

“A top this month would certainly make sense to us given the recent overbought conditions, unsustainably high bullish sentiment levels, bear capitulation (not Crescat), and deteriorating macro indicators,” Smith wrote, indicating that the mid-January highs might be as good as it gets for a long while.

He continued, warning that “investors will need a good grounding in valuation and business cycle analysis to reject the common buy-the-dip advice that is soon to become prevalent in the still early stages of what is likely to become a brutal bear market.”

Tavi Costa, Crescat portfolio manager and co-writer of Smith’s note to clients, later tweeted that the current stock valuations are “truly insane.”

“The median EV to Sales ratio for the stocks is now 3.6x,” Costa wrote, reiterating Crescat’s position in Smith’s note. “Twice as high as it was at the peak of the tech & housing bubbles. The breath of valuations has never been so frothy.”

Costa also attached a chart, similar to the one produced by Smith. Since 2013, the median EV-to-sales of S&P 500 companies has effectively “broken out,” far surpassing what it was in the decade prior.

Given the current valuation data, it’s hard to argue with Smith and Costa. Equities certainly appear overvalued according to the EV-to-sales ratios. The coronavirus outbreak – an event identified by many bears as a “trigger point” for the next crash – could cause stocks to sink much like SARS did in 2003, when the major indexes dropped double digits in a matter of weeks.

Back then, however, the median EV-to-sales ratio was less than half of what is now. Stocks, in essence, had less value to “shed” during a correction. These days, there’s arguably way more room to fall.

But like with all other doomsday predictions, there’s no use getting worried until the serious selling actually begins. Noted perma-bear (and gold bug) Peter Schiff has been predicting a financial collapse for decades now.

He was right, of course, back in 2008, but that was one correct prediction out of many. By taking his advice and avoiding the market since, investors would’ve missed out on the longest bull run in history.

Compared to Schiff, Smith and Costas come better-equipped with much more compelling data. But until investors smell blood in the water, the market will likely keep rising. Bulls have shown over the last few years that valuations don’t really matter; companies just need to keep beating quarterly earnings estimates.

That doesn’t mean investors should run out and “buy the dip.” But it also doesn’t mean they should leave the market entirely, either.

The S&P exploded for a 28% gain last year, after all. In 2020, it’s trading “flat” after enjoying a meteoric rise. And even with the coronavirus running China ragged, stocks aren’t in correction territory quite yet. Instead of trying to predict the future with EV-to-price ratios, it might be more prudent to simply follow the charts.

It’s a strategy that kept bulls invested in 2019, when the market logged a near-historic gain. Don’t forget that around this time last year, analysts were predicting a major economic slowdown and correction – something that never happened. If the U.S. stock market can survive – and even thrive – during a protracted trade war with China, the coronavirus doesn’t stand a chance.

{kind=link}