Stocks are falling this morning as lockdowns sweep across Europe. European stocks dropped, too, reflecting investor fears over a Covid-19 mutation that’s more resistant to the current vaccines. With equities having just hit new all-time highs, the rally isn’t in danger of collapsing just yet.

It could, however, be weakening. And that has Wall Street a little nervous about the rampant bullishness given today’s investing climate.

“There are two types of investors: those who want to get rich, and those that want to stay rich,” wrote Bank of America analysts in a note to clients.

“When those who want to stay rich start acting like those who want to get rich, it suggests a late-stage speculative blow-off.”

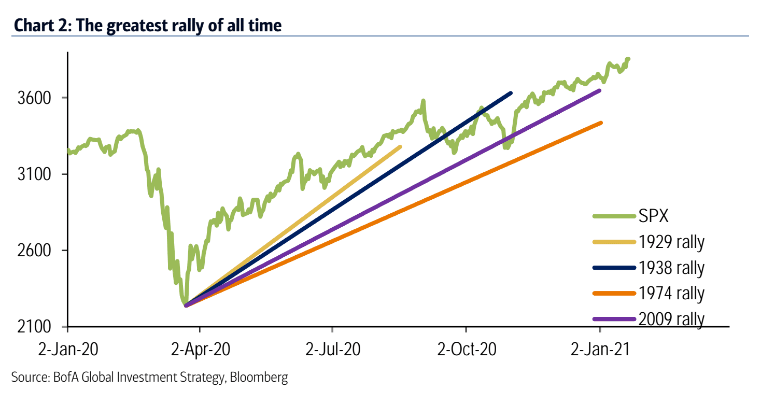

Irrational exuberance has helped put the S&P 500 (as represented by the SPX) ahead of the mega-rallies prior, but investor optimism hasn’t been completely unfounded. Unprecedentedly accommodative fiscal policy ensured that the short-term future would be “backstopped.”

It gave bulls, of both the retail and institutional variety, major buy signals week after week.

Now, though, a mutant Covid strain may have changed the rules of the game, along with mounting inflationary risks.

“Extreme policy remains [the] best explanation for extreme rally off lows in 2020,” said B of A analysts.

“But Wall Street inflation will likely drag Main Street inflation higher, risking disorderly rise in bond yields (taper tantrum), tighter financial conditions, [and] volatility events.”

The note then reeled off several major market meltdowns, all of which resulted from bond yield and inflation uncertainty. That list included the infamous Dot Com and Housing Bubbles, as well as 2018’s rate hike folly that sunk stocks toward the end of the year.

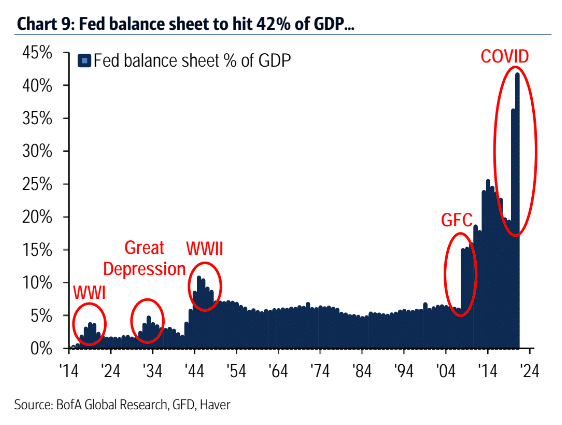

Perhaps the most shocking statistic provided by B of A was the size of the Fed’s balance sheet, which has quickly mushroomed to a whopping 42% of GDP during the pandemic.

Anyone up to date on financial news knows that the Fed’s providing liquidity at a large scale. But it’s hard to grasp just how much liquidity there is without a comparison to the Fed’s bond-buying programs of years past.

Many analysts thought the 2008 Financial Crisis would represent the peak in that regard. Roughly five years later, the Fed expanded its balance sheet further, hitting roughly 25% of GDP.

Then, in 2020, the balance sheet additions went parabolic. It seems impossible that the Fed could go any higher from here, but if its post-Financial Crisis behavior is a valid indicator, we may see a 50%+ GDP balance sheet in the coming years.

So, where does that put stocks? Likely in a highly precarious position – something Wall Street continues to acknowledge in its research reports.

And yet, nearly every bank is still long equities in a major way. According to the December Fund Managers Survey, they think that tech stocks are the most overcrowded sector in the market.

But in January, they’re buying tech again. Retail investors are, too. Especially now that renewed Covid uncertainty is stinging value shares.

Overall, the evidence against a bullish continuation is accumulating rapidly. That does not, however, mean the good times are finished just yet. Until stocks string together several negative trading sessions in a row, bulls should remain in control.

Even if bears – frustrated as they may be – have every reason to anticipate a market-wide crunch.

{kind=link}