Stocks are falling today as investors digest several bearish signals. For the week ending February 12th, the U.S. added 861,000 new unemployment fillings, beating the Dow Jones estimate of 773,000. It’s also the highest weekly jobless claims reading that the market has seen in roughly a month.

A labor recovery slump – something bulls seemed to have written off completely over the last few weeks – could wreak havoc on equities moving forward.

“This is not the direction that you want to see jobless claims go but keep in mind this could be a small bump in the road as the pace for vaccinations continues to accelerate and cases are down across the country,” said E-Trade Financial CIO Mike Loewengart.

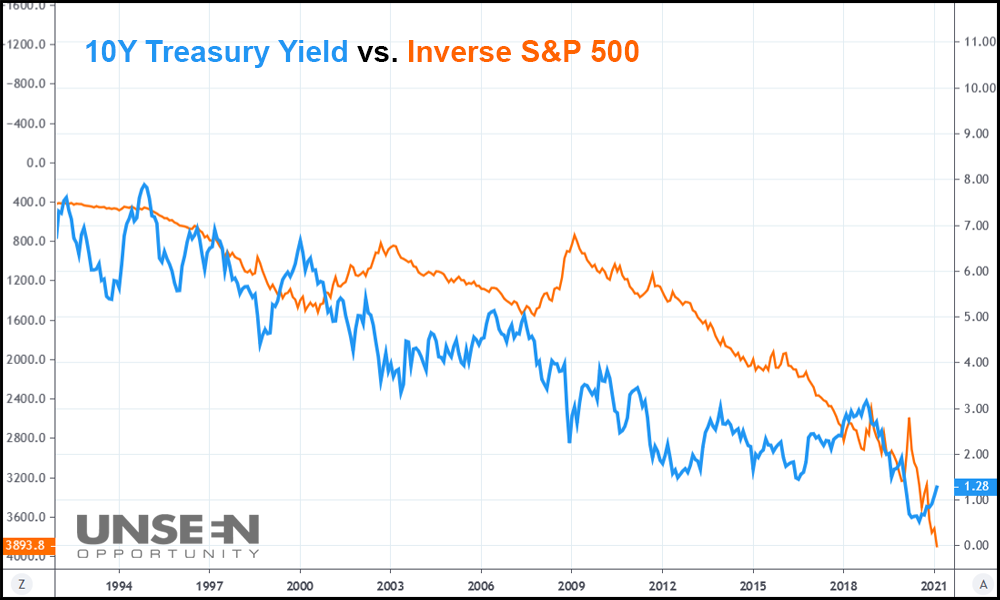

But it’s not just unemployment data that has investors feeling down this morning. The 10 Year Treasury yield is back up again today, hovering near 1.3% en route to what could be an even steeper bond sell-off.

The previous high of 1.20% held for several weeks. On Tuesday, however, the 10Y yield soared to 1.3%, breaking past a key level of resistance as Treasury notes sunk.

This downtrend in Treasuries (and uptrend in yields) is on a path that’s potentially very bad for equities. Rates expert and Nomura strategist Masanari Takada warned clients about this in a note from yesterday.

“[I] also envision a risk scenario in which [commodity trading advisors’] move to the short side in [U.S. Treasury] futures (TY) becomes essentially unstoppable, pushing the 10yr yield to above 1.5% and forcing US equities (the S&P 500) to adjust downward by 8% or more,” he said.

We’re not there yet, but the higher the 10Y yield goes, the worse it will get for stocks. Anything above 1.4% would likely cause some reactionary selling. If the 10Y yield hits 1.5%, Takada’s 8%+ correction prediction certainly seems possible.

It’s all being driven by commodity trading advisors (CTAs) that are dumping Treasury notes. According to Takada, the CTAs think the global economy is going back to its pre-trade war state. They’re buying-up copper futures (and other commodities) as a result, eschewing the 10Y notes for soon-to-be in-demand materials.

Historically, the 10Y Treasury yield has moved in the opposite direction of the market. The lower yields drop, the higher stocks go.

In late 2018 when Fed Chairman Jerome Powell attempted to induce quantitative tightening (QT), the 10Y yield jumped out of its longer-term downtrend. The S&P 500 corrected over 17% in response.

These days, the 10Y yield is exhibiting similar behavior. It’s currently on track to break out past 1.4% sometime in March.

If that happens, late-2018-like selling could follow, potentially dwarfing even Takada’s 8% equity crunch prediction while the U.S. continues to recover from Covid-19.

{kind=link}