Stocks traded flat this morning as investors did some soul searching. Bulls have pushed the market to dizzying heights over the last few weeks, escaping a minor February correction in the process. It’s been mostly good news since the S&P broke new ground on April 1st. On April 5th, a stunning March jobs report (released on Good Friday) sent equities higher.

Even last week’s worse-than-expected jobless data was unable to derail the rally.

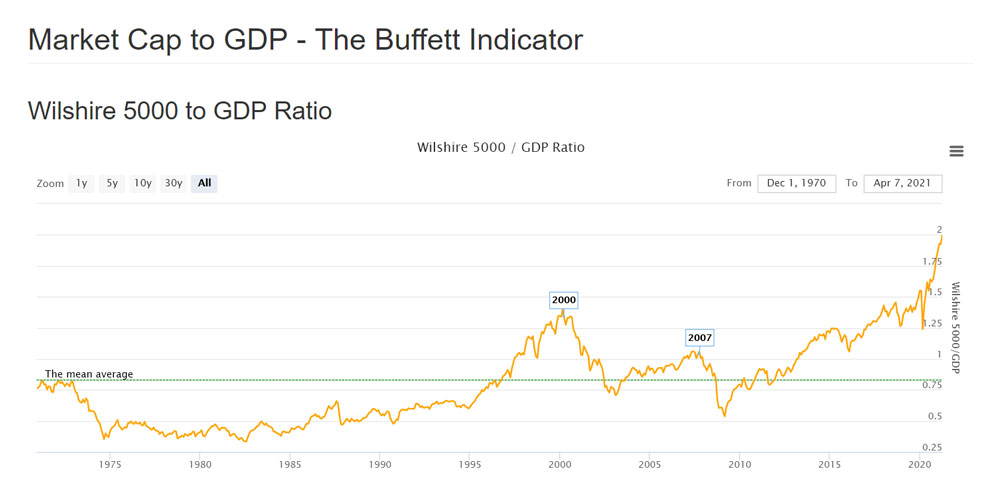

The result is yet another new record for the “Buffett Indicator,” which charts the Wilshire 5000’s market cap against U.S. gross domestic product (GDP).

Warren Buffet said in 2001 that “it is probably the best single measure of where valuations stand at any given moment.” Currently, there appears to be a major disconnect between the market and the economy.

As a timing mechanism, though, the Buffett Indicator isn’t all that accurate. It tends to cross its mean average well ahead of market lows. In 2013, Buffett himself admitted that “it’s not that precise,” and was more fitting during the early 2000s following the dot-com bubble.

In short, investors shouldn’t use it to make buy/sell decisions. But that doesn’t mean it should be ignored entirely, as it can provide a rough “snapshot” of how far apart current economic conditions and future expectations truly are.

The gulf between the two has grown to historic levels in 2021.

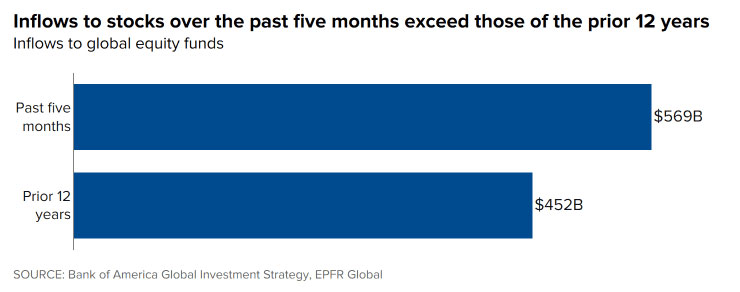

Supporting the “over-bullishness theory” is another shocking statistic revealed on Saturday by Bank of America.

Market inflows are hitting unprecedented levels as well. It’s not all that surprising given how high stocks have soared, but it’s still extremely disconcerting to anyone holding long positions.

The last time the S&P went on a run of this magnitude (+3.4%) above an all-time high was in September 2020, when the market soared roughly 5% in just 8 trading days.

A 10% peak-to-trough correction immediately followed.

Does the same fate await investors this week? It certainly seems possible, if not probable, considering how high valuations currently are. But unlike in September, economic conditions are improving rapidly. Nearly every investor – from Wall Street to Main Street – is anticipating an economic boom.

Liquidity, stimulus, aggressive fiscal policy, and reopenings are likely to provide that in short order. The Fed wants higher inflation.

They’re going to get it in spades if things continue on their current track.

However, bulls won’t pull back until it reaches worrying levels. And chances are that tomorrow’s consumer price index (CPI) reveal won’t reflect anything close to that, thanks to the Bureau of Labor Statistics’ inability to gather accurate data. The last few CPI readings used estimated numbers. Tomorrow’s is unlikely to be much different.

And even if the CPI creeps higher than expected, earnings season could wash away many inflation-related fears. The market’s top stocks are expected to report big quarterly results.

If they do, bulls will get the confirmation they need to keep buying. But if they don’t? Who cares. The Fed’s going to keep things “easy-breezy” indefinitely.

Which could mean more gains for long traders, defying the Buffett Indicator for another nauseating few weeks at the top of the market.

{kind=link}