September is here and the market is still falling. Stocks tumbled again today as September got off to a bearish start. The Dow dropped 0.5% while the S&P sunk 1.1%. Tech shares led the market lower, dragging the Nasdaq Composite down to a 2.2% loss.

Sentiment went from bullish in early August to downright apocalyptic over the last week after Fed Chairman Jerome Powell’s speech last Friday sparked a shocking one-day selloff. Since then, however, bearish sentiment has continued to “snowball.”

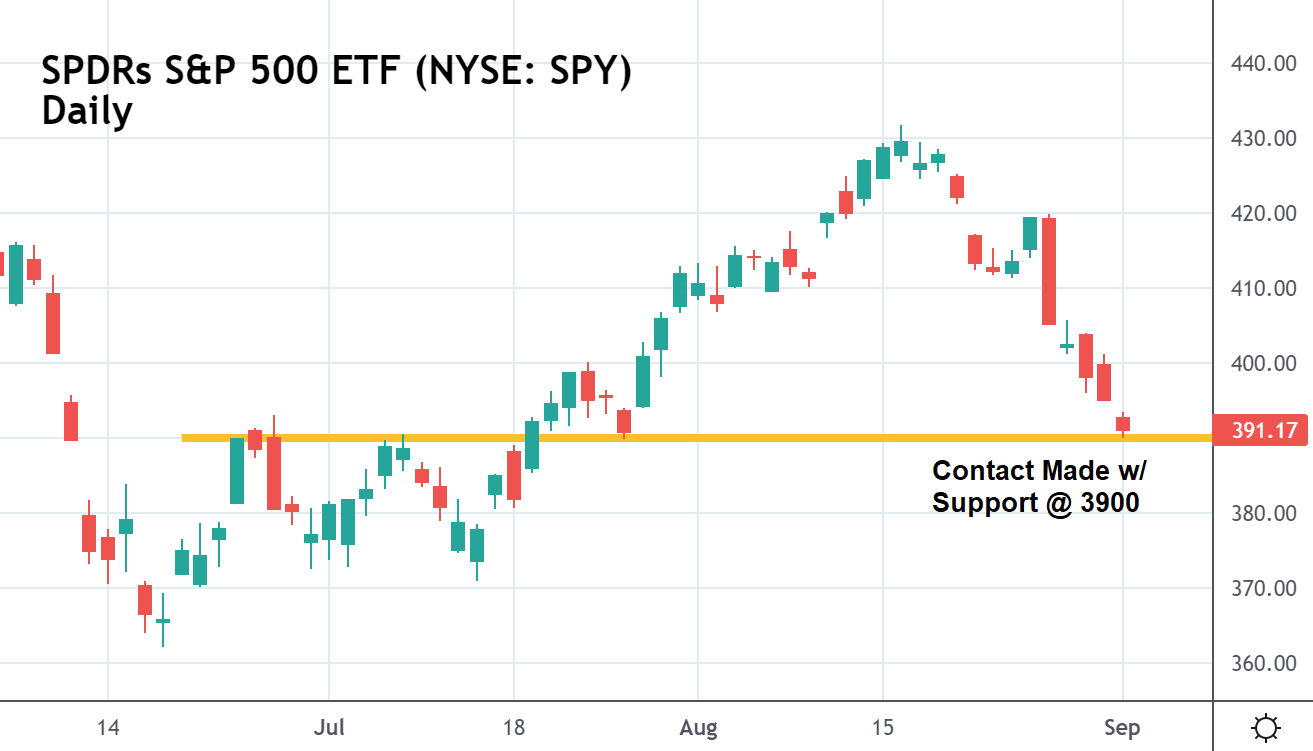

And it might only get worse from here as the market enters a historically bad month for bulls. The only thing standing in the way of a deeper correction is S&P support at 3,900 at the late June/early July highs.

Earlier this morning, the S&P (as represented by the SPY above) temporarily touched 3900 before bouncing slightly higher. The broader market index remains down on the day.

Many analysts see 3900 as the market’s last line of defense protecting stocks from retesting their June lows.

“Many metrics are flashing oversold signals, which combined with meaningful support around 3,900 suggests the bulls ‘should’ be able to stage a rally here,” said BTIG chief market technician Jonathan Krinsky.

“Given this set-up, should they fail to hold 3,900, we would have to say the June lows were back in play.”

Krinsky’s right in that stocks do look very oversold in the short-term. A bullish bounce seems imminent.

Whether the coming rally can keep its gains, however, is another story. Quantitative tightening by the Fed and a refusal from Powell to pivot dovish have investors viewing the market’s outlook much differently now.

That means the precipitous selloff of the last week is likely to resume even if bulls can stage another (probably short-lived) bear market rally soon.

“Optimism around a soft landing and [first half 2023] rate cuts has diminished following Jackson Hole, and there are still no real signs of a new bull market yet,” said Savita Subramanian, Bank of America’s head of US equity and quantitative strategy, in a note to clients.

The market’s next major sell (or buy) trigger is coming tomorrow with the release of the August jobs report.

“Let’s face it, the rise in long-term rates has been a leading reason for the recent decline in the stock market,” said Miller Tabak’s Matt Maley.

“[The jobs report could have a] critical impact on those long-term rates […] at least when the report is different than consensus expectations.”

Strategists are sticking with the “bad news is good news narrative.” A soft jobs number, they say, would be good for stocks as it would give the Fed an excuse (weakening labor) to go with smaller rate hikes.

Several days ago, however, we discussed how the Fed is unlikely to be persuaded by bad jobs reports. Powell made it clear in his speech last Friday that defeating inflation now trumps all other pursuits, including a strong labor market.

That means good news will be bad news and bad news might also be bad news, leaving bulls in a very difficult spot with critical support in range of another bearish blast lower.

{kind=link}