Stocks fell through noon today following a wild morning session due to a hotter-than-expected inflation reading. The Dow, S&P, and Nasdaq Composite all slipped while yields climbed. The 10-year Treasury yield advanced to almost 3.8%, hitting a 40-day high. The 6-month Treasury yield is on track to close above 5% for the first time since July 2007.

The January Consumer Price Index (CPI) – released before trading opened this morning – was to blame for the yield rip and stock dip. Headline CPI increased by 6.4% year-over-year (YoY) last month vs. 6.2% expected. Month-over-month (MoM), headline CPI climbed 0.5% vs. 0.4% expected.

Core CPI, which excludes food and energy prices, surpassed estimates as well. Core climbed 5.6% YoY vs. 5.5% expected and 0.4% MoM vs. 0.3% expected.

Overall, it was a slightly hotter-than-expected print. Wall Street analysts twisted themselves up in knots trying to explain why this was still somehow bullish after telling clients last week that the market had significant additional upside.

“While there were no major surprises in today’s CPI reading, it is a reminder that while inflation has peaked it could be a while before we see it moderate to normal levels,” said Morgan Stanley portfolio chief Mike Loewengart.

“The question remains if inflation will be able to fall to the Fed’s target levels with the labor market as tight as it currently is. That could be the recipe for a soft landing, but it remains to be seen when the Fed will shift away from rate hikes and if the labor market will lose its resiliency.”

Jeffrey Roach, chief economist at LPL Financial, offered a far soberer (yet still slightly optimistic) take on the data.

“Inflation is easing but the path to lower inflation will not likely be smooth,” Roach said.

“The Fed will not make decisions based on just one report but clearly the risks are rising that inflation will not cool fast enough for the Fed’s liking.”

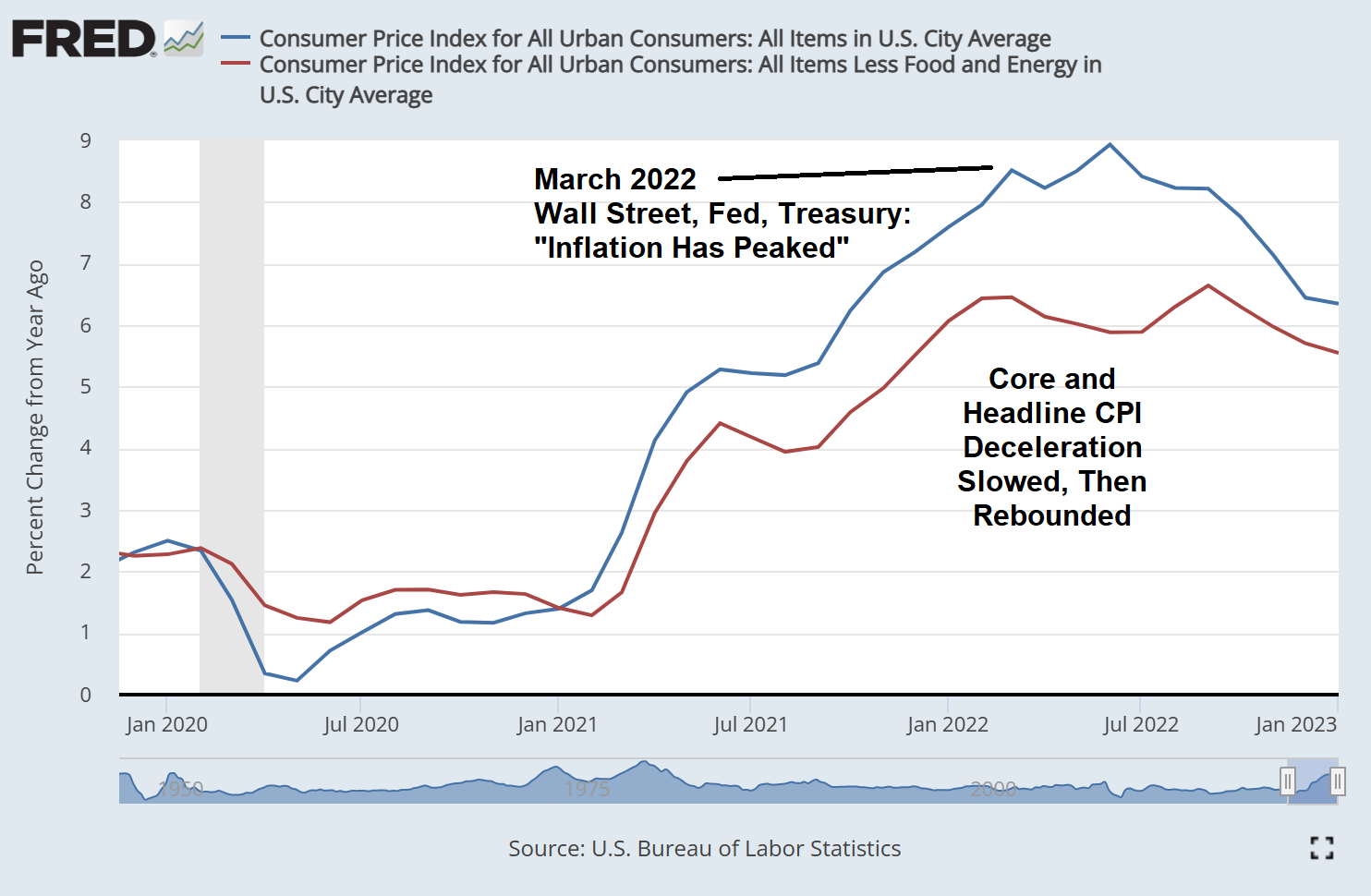

Alternatively, it’s clear now that inflation is no longer falling like it once was. Wall Street, the Fed, and the US Treasury all had prominent experts declaring that inflation had peaked back in March 2022. Headline and core CPI fell before rebounding sharply to set new highs.

The experts were wrong. These are also the same folks who said high inflation was merely “transitory” in 2021.

That’s not to say we’re definitely going to see inflation bounce higher again, but that same early 2022 pattern is forming. Analysts also are starting to act like everything’s going to be just fine for the US economy.

Meanwhile, egg prices were up 70.1% year-over-year as of last month.

And so, the experts have an opportunity here to outdo themselves by upgrading their “double wrong” track record (inflation is transitory, inflation has peaked) to “triple wrong” (the disinflation process has begun) if inflation remains stubbornly high.

January’s data was the first indication of that, which is not what bulls wanted to see at the top of an already impressive multi-week rally. With little else to look forward to this week, traders will have plenty of time to wonder whether today’s CPI release marked the end of the bear market melt-up.

{kind=link}