Stocks rose moderately this morning on hopes that the banking crisis ended over the weekend. The Dow and S&P both gained while the Nasdaq Composite traded flat through noon. Regional banks were among the day’s biggest winners after plunging in the week prior.

Last night, UBS struck a deal with Credit Suisse to purchase the beleaguered bank for $3 billion. UBS didn’t necessarily want to do this, but it was a better alternative than letting Credit Suisse fail, as it would have crashed global banking shares with it.

The “shotgun wedding” was backstopped by the Swiss National Bank, which provided 100 billion francs in support of the deal. That’s the second time the banking industry prevented a catastrophic collapse over the last few days; the first was the $30 billion bailout of First Republic Bank by a group of 11 major American banks on Thursday.

And though it’s nice to see the private sector patch its own holes, the comingling of banks could also be exposing otherwise healthy banks to substantially more risk than before. That has investors hesitant to buy the dip, especially with a rate hike coming up on Wednesday.

“I think there’s a pendulum that swings too far each way,” said Jeff Kilburg, CEO of KKM Financial.

“Last week, there was a punishment and a range of emotion — really exaggerated — the selling as well as the buying. People are reminiscing on what happened. So that was the initial fear, even though Silicon Valley Bank is not a Lehman moment.”

It may not have been the “Lehman moment” bears were betting on but was it something else?

In JPMorgan’s morning briefing to clients, the bank’s analysts addressed the banking crisis.

“Is the banking crisis over? The short answer is Maybe. Our Financial Sector research teams do not see elevated risks of contagion as they view recent events as idiosyncratic. Short-term [Fixed Income Clearing Corporation] funder markets are not experiencing stress as liquidity conditions are not as dire as [the Global Financial Crisis] or peak-COVID.”

The note continued:

“However, there are multiple media outlets reporting that several banks are putting restrictions on trading with at-risk banks […] Combined, actions this weekend and this week will likely support the immediate risk from the 4 banks across US/EU; but investors may continue to see 2008 as an analogue.”

On whether this is a financial crisis-like event or not, the bank asked:

“If what we have is Bear Stearns, then what is the Lehman event?”

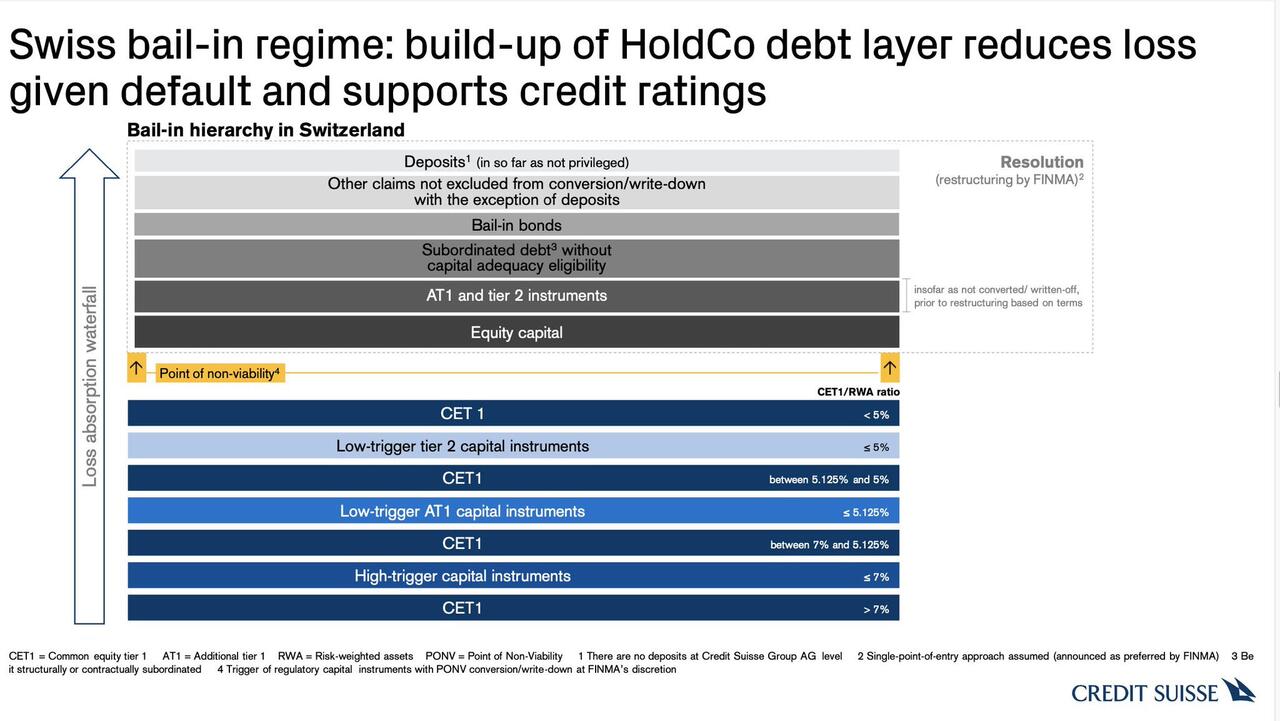

It could be the European bond chaos that’s taking place as a result of the Credit Suisse sale. As part of the deal with UBS, all Credit Suisse Additional Tier 1 (AT1) bonds were written down to $0. That wiped out $17 billion of Europe’s total $275 billion AT1 bond market in a single moment.

AT1 bonds are also called “contingent convertibles” (or “CoCos” for short) and were created following the Global Financial Crisis in 2008 as a “shock absorber” for banks. The idea was that AT1 bonds would make government-funded (ie, taxpayer-funded) bailouts a less common occurrence.

That means AT1 bonds are risky, as they’re converted to equity or written down to $0 in a time of crisis. Credit Suisse did the latter yesterday despite the fact that shareholders should theoretically suffer losses before AT1 bondholders during a typical writedown.

Because AT1 bonds are risky, they offer higher yields than other bonds of a similar credit rating. That makes them popular with institutions.

This is an issue, of course, as these AT1-holding institutions are pillars of the global financial structure. Institutional investors balked at the sale of Credit Suisse, which is about to return $3 billion to shareholders while leaving AT1 bondholders with nothing.

“This just makes no sense,” said Aquila Asset Management’s Patrik Kauffmann, who is stuck with a glut of worthless Credit Suisse CoCos.

“Shareholders should get zero […] it’s crystal clear that AT1s are senior to stocks.”

European regulators swooped in this morning and reassured investors that any future bank mergers would cause shareholders to suffer losses before AT1 bondholders. What happened with Credit Suisse, they said, was a fluke as Credit Suisse did not first consult the European Central Bank’s (ECB’s) Banking Supervision wing due to how quickly the deal formed.

It ultimately came down to the Swiss National Bank, which prioritized shareholders over AT1 bondholders. Italian Finance Minister Giancarlo Giorgetti said he was “surprised” by the decision to do so.

The market didn’t seem too happy with the ECB’s “reassurances,” as evidenced by a plunge in risky European bank debt today. Most European banks saw their AT1 bonds fall to record lows.

So, are AT1 bonds going to provide the next “Lehman moment?” Will AT1s be looked at in a similar way as collateralized debt obligations (CDOs)?

To echo JPMorgan this morning: “Maybe.”

If that turns out to be the case, the banking industry will only have itself to blame yet again, as AT1s are a purely synthetic creation in response to the Global Financial Crisis. And, ironically, they could serve as the catalyst for another one. Time will tell.

{kind=link}