Stocks continued their rally today, attempting to recover from a three-month downward trend. The focus was primarily on the bond market and the anticipation surrounding the Federal Reserve’s October/November meeting. Or, more accurately, Fed Chair Powell’s post-FOMC press conference. The S&P 500 saw a rise of 0.2% shortly after the market opened, with the Dow Jones Industrial Average remaining relatively stable. Meanwhile, the tech-centric Nasdaq advanced by 0.3%.

Investors are keenly awaiting the Federal Reserve’s interest rate decision, expected later today. The consensus is that the central bank will maintain the current rates but will keep the door open for potential hikes if deemed necessary. Market participants will be closely analyzing the Federal Reserve’s statement and Powell’s remarks for insights into the future trajectory of interest rates. The overarching sentiment is that officials will proceed with caution to ensure the U.S. economy doesn’t decelerate significantly while addressing inflation concerns.

In the bond market, Treasury yields experienced a slight decline, with the 10-year yield hovering around 4.87%. This shift occurred after the US Treasury’s announcement of a $112 billion debt auction next week, aligning with market predictions. This announcement has garnered increased attention from stock investors, especially considering its potential influence on the recent surge in yields.

On the employment front, the ADP National Employment Report for October indicated the addition of 113,000 jobs, falling short of the anticipated 150,000.

In the midst of the ongoing earnings season, AMD’s shares dipped despite surpassing estimates, primarily due to its Q4 guidance. Kraft Heinz reported sales that didn’t meet Q3 expectations, while CVS showcased impressive profits, largely attributed to its robust pharmacy segment. Given that investors don’t expect much out of Powell today, earnings should continue to drive broader market sentiment.

That was true in October as the “Magnificent Seven’s” earnings were mixed, causing divergences among the market’s top names. Steve Sosnick, Chief Strategist at Interactive Brokers, commented, “At this point, you can’t look at them as seven stocks together.” Notably, Amazon and Microsoft reported significant growth in their cloud services, surpassing investor expectations. In contrast, Alphabet witnessed a decline in its stock value following underwhelming cloud business results. Nvidia faced challenges due to potential restrictions on AI chip exports to China by the Biden administration. Tesla’s stock value decreased after reporting lower-than-expected profits, raising concerns about the adoption rate of electric vehicles.

The valuation of these tech giants has been a topic of discussion, especially in light of the Federal Reserve’s interest rate outlook. Steve Sosnick highlighted the risks, stating, “These stocks are expensive and it’s not like you’re taking a risk on a stock that’s got a very affordable valuation.”

Investors have noted that a significant portion of the S&P 500’s gains this year can be attributed to these dominant tech stocks, which make up roughly 30% of the index’s market cap. However, this momentum can also reverse. Charles Schwab Chief Markets Strategist, Liz Ann Sonders, emphasized the influence of these stocks on the S&P 500, suggesting that the index’s movement can be directed by their performance.

Sonders also mentioned that a more balanced market rally isn’t solely dependent on these major players. She stated, “If you start to see better breadth [outside the Magnificent Seven], I would view that as a positive.” While there have been indications of a broader market trend, it hasn’t fully materialized.

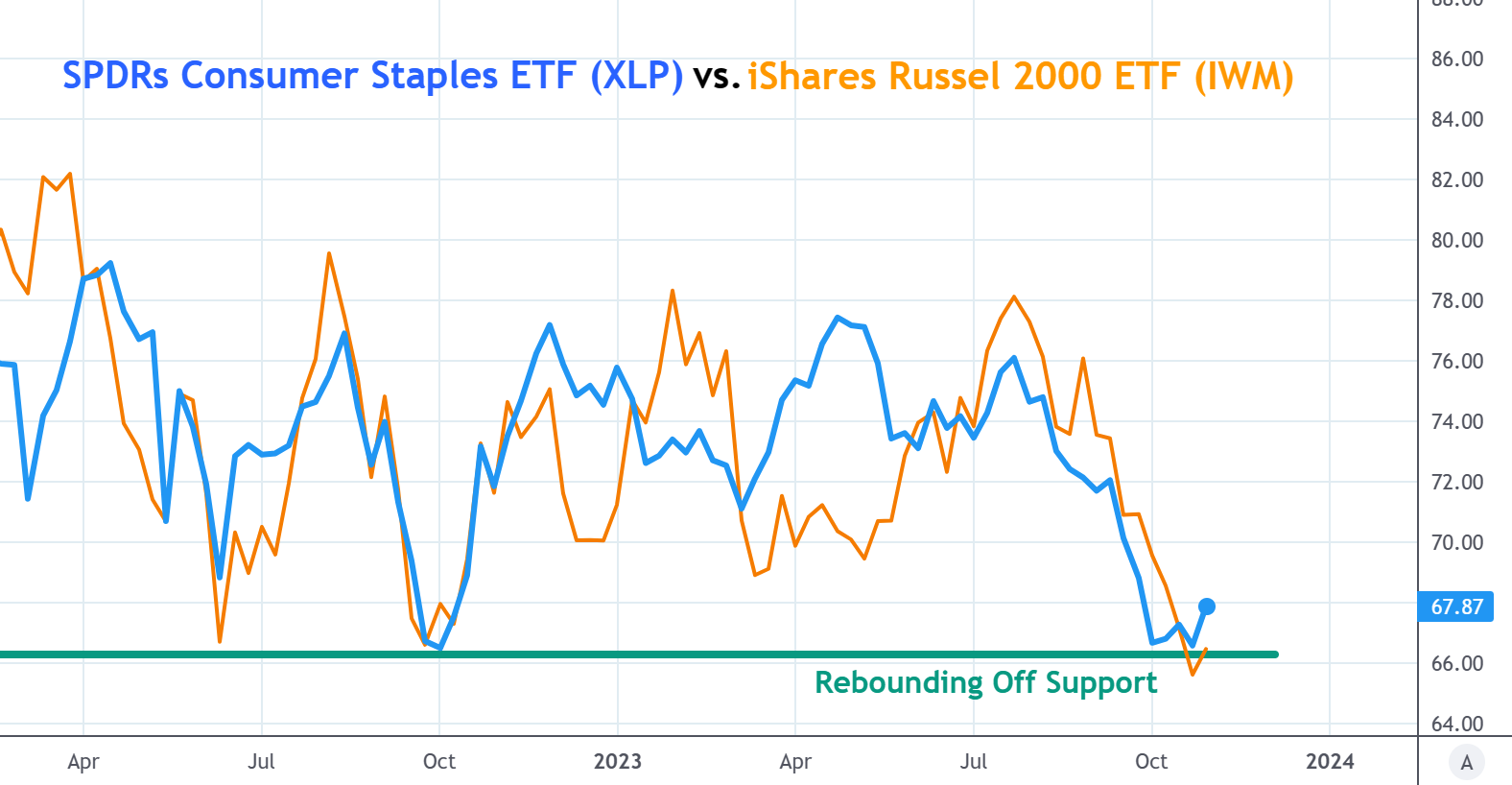

The Russell 2000 recently reached its lowest since October 2022. Financials are still trailing by over 5% this year. Even strong earnings reports haven’t significantly influenced the market.

Sonders further commented on the market’s performance over the past year, “There’s a lot that is lacking about what the market has done in the past year and all you have to do is look under the surface of some of those biggest stocks to see what some of those missing links are.”

As the influence of the Magnificent Seven wanes, it’s becoming evident which market sectors might have been underprepared during the 2023 rally. The challenge now is determining which sectors are best poised for recovery.

“Junk food” brands in the consumer staples sector seem to be likely overachievers after getting crushed by shorts over the last few months. The aforementioned Russell 2000 could be a good pick, too, considering how much it’s underperformed the S&P. If a rally’s really on its way, there may not be better buys than the SPDRs Consumer Staples ETF (XLP) and the iShares Russell 2000 ETF (IWM), both of which are trading on support levels formed in late 2022.

{kind=link}