Stocks slipped today following a choppy morning session. The Dow, S&P, and Nasdaq Composite all traded slightly lower to start 2023 on a frustrating note. Tesla (NASDAQ: TSLA) and Apple (NASDAQ: AAPL) led the market lower, falling 11% and 3.50%, respectively, through noon.

Before the market opened, though, S&P futures were up as much as 1%, stoking bullish confidence. Shares then plunged across the board within the first 30 minutes of trading as stocks resumed their short-term bearish trend that began in mid-December.

Some analysts expect other market trends from 2022 to continue this year as well.

As we kick off 2023, it may be worth taking another look at 2022, which saw Q4 produce the only positive quarterly returns of the year,” wrote JPMorgan strategists in a morning brief.

“Somewhat surprisingly, the [S&P 500] posted a positive return with Tech still underperforming (both NDX and Nasdaq were negative for 22 Q4). Value and Defensives were the standouts.”

The bank’s analysts then asked whether this trend – underperformance from tech opposite overachieving value stocks – would last.

“Yes. As long as the Fed remains active the US likely remains in a bear market,” the note read.

“While some investors are ‘looking through’ inflation those whose investment horizon is 12 months or less are unlikely to try to get ahead of the Fed. The Fed tends to maintain a tightening cycle until Fed Funds exceeds headline inflation.”

November’s CPI, the most recent consumer inflation report, showed a headline inflation rate of 7.1%. The fed funds rate is currently 4.25%-4.50%. Bulls are hopeful that demand destruction via a recession will bring inflation below 5.1% (the Fed’s median rate for 2023). And though a recession would certainly reduce demand, it wouldn’t soak up all the cash that was injected into the US economy over the last three years.

In the same morning brief, JPMorgan strategists predicted an April CPI print of 4.5%, bringing the inflation rate below what the fed funds rate is projected to be at that time (4.75%-5.00%).

History suggests that this would end the Fed’s hiking cycle. If, however, inflation doesn’t fall as quickly as expected, the Fed would theoretically keep rates elevated into H2 2023.

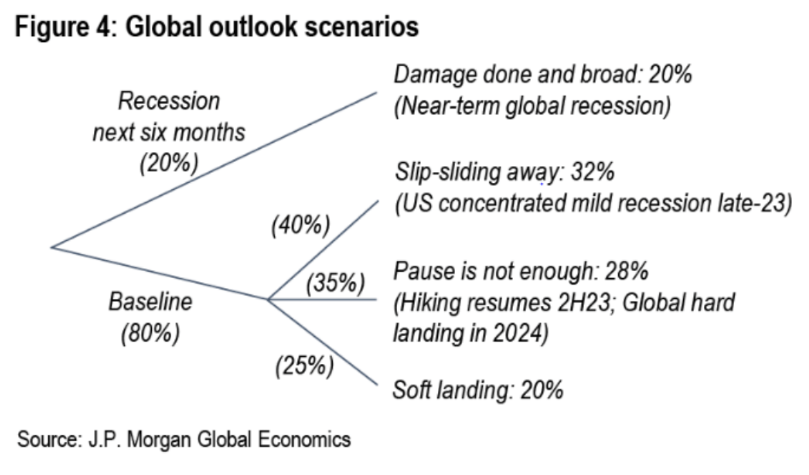

As laid out by JPMorgan analyst Bruce Kasman, however, a tight labor market could prompt additional restrictive action from Powell & Co. even if inflation abates.

“We expect the global expansion to display resilience and divergence as we turn into 2023 but do not anticipate a soft-landing. The inflation slide should encourage a central bank pause but is unlikely to be complete. Tight labor markets will warrant sustained restrictive stances, tighter credit conditions, and a gap between waning corporate pricing power and sticky labor costs,” Kasman said.

JPMorgan’s only projected “good” outcome is a soft landing for the US economy, which the bank says has a 20% chance of occurring. Everything else involves a hard landing, with the worst-case scenario being an imminent global recession within the next six months.

Ironically, traders would probably prefer the doomsday option here as it would flush equities down the drain in one fell swoop vs. a slow crawl lower. Either way, the bear market will last well into 2023 as JP Morgan’s analysts correctly observed this morning.

The sooner the house of cards comes crashing down, the better. That would pave the way for rate cuts and another potential “mega rally” akin to 2020-2021.

But cutting rates would also likely coincide with the Fed raising its inflation target, which is currently 2.0%. It typically takes developed economies (like the US) about 10 years for inflation to fall to 2.0% after it jumps above 5.0%. The US eclipsed 5.0% inflation in June 2021 (+5.3%). On that timeline, inflation won’t fall to the Fed’s current target until June 2031.

This suggests that, pending an economic miracle, the Fed will eventually lift its inflation target. When it does, bulls will celebrate. But long-term buy-and-hold investors will be left disappointed as inflation eats into their real market gains, potentially even transforming their nominal returns into losses as stagflation takes hold.

{kind=link}