Stocks traded flat again this morning as investors prepared for the latest batch of jobs data. The Dow and S&P both remained mostly unchanged through noon while the Nasdaq Composite held on to a small gain.

Tomorrow morning, the Bureau of Labor Statistics (BLS) will release the February jobs report. Heading into the report, conflicting data made estimating tomorrow’s print a difficult affair. ADP reported better-than-expected private payrolls yesterday, which suggests that investors will see a strong jobs number from the BLS.

But according to analytics firm Challenger, Gray, & Christmas, US-based employers announced 77,770 job cuts last month, representing a massive 410% year-over-year increase compared to the 15,245 cuts in February 2022. This number was actually down from January’s 102,943 job cuts.

That’s 180,713 jobs total between January and February, which is the most for the two-month stretch since 2009.

“Certainly, employers are paying attention to rate increase plans from the Fed. Many have been planning for a downturn for months, cutting costs elsewhere. If things continue to cool, layoffs are typically the last piece in company cost-cutting strategies,” explained Andrew Challenger, Senior Vice President of Challenger, Gray & Christmas.

“Right now, the overwhelming bulk of cuts are occurring in Technology. Retail and Financial are also cutting right now, as consumer spending matches economic conditions. In February, job cuts occurred in all 30 industries Challenger tracks.”

Having to go back to the Global Financial Crisis to see similar job cut data is not an auspicious sign. But will those cuts make an impact on the February jobs report? Most investors aren’t ready to take that bet.

“It’s going to be choppy trading with not a lot of volume because no one wants to pick up nickels in the face of a potential bulldozer with Friday’s jobs report,” said Wells Fargo strategist Paul Christopher.

As we’ve seen in recent jobs reports, a dramatic uptick in part-time hospitality jobs (bars, restaurants, hotels, etc.) has covered for falling full-time, corporate payrolls. Traders won’t see another massive +517k jobs print tomorrow like in January’s report, but the February tally could still easily come in above consensus as actual layoffs lag announced job cuts.

ADP’s report yesterday was a major indicator of this. So too was the Job Openings and Labor Turnover Survey (JOLTS), which revealed a higher-than-expected number of job openings. Like with the rest of the labor market’s data, however, JOLTS findings continue to look suspect. Only about 30% of the JOLTS requests are returned by respondents these days, meaning that the other 70% of the JOLTS data is the result of an estimate.

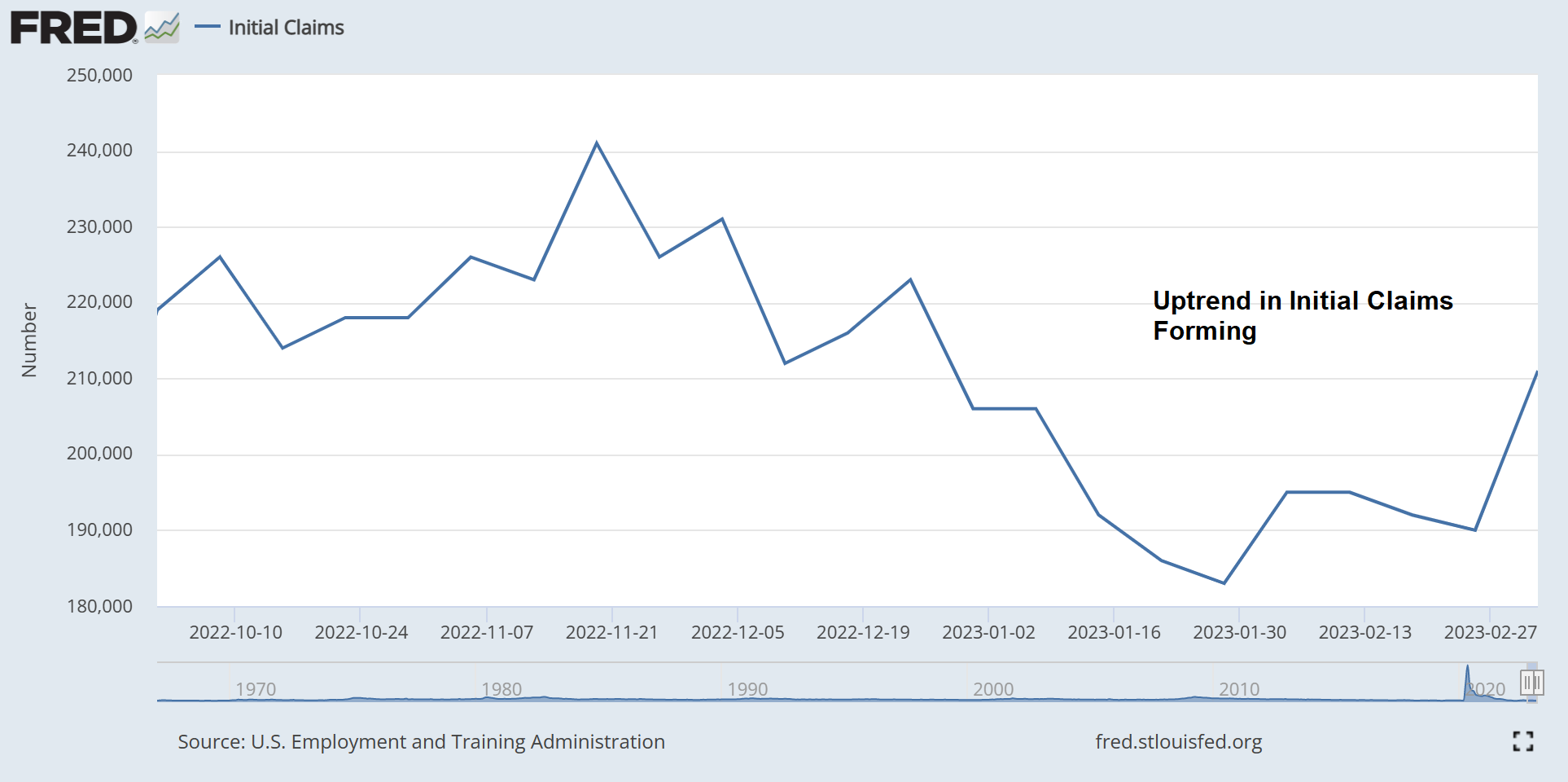

Nonetheless, a clear trend has formed leaning toward a hot jobs report for February but a very weak one in March. Weekly initial jobless claims released this morning suggested that as well, showing a sudden uptick for the week ending March 3rd.

First-time unemployment filings clocked in at 211,000, hitting a high unseen since December 24th, 2022. Continuing claims, meanwhile, advanced to 1.718 million for the week of February 25th, matching the December 17th high.

The weekly unemployment data prompted a note from Goldman Sachs chief economist Jan Hatzius, who wrote that “seasonal adjustment issues have exerted an increasing amount of downward pressure on initial claims over the last few months” and “the pressure will begin to reverse in a few weeks.”

January’s jobs report enjoyed the largest seasonal adjustment of all time. January 2022’s jobs report was the prior record holder. As noted by Hatzius, though, the seasonal adjustments could soon “rubberband” lower, pumping up initial claims while dragging down added payrolls.

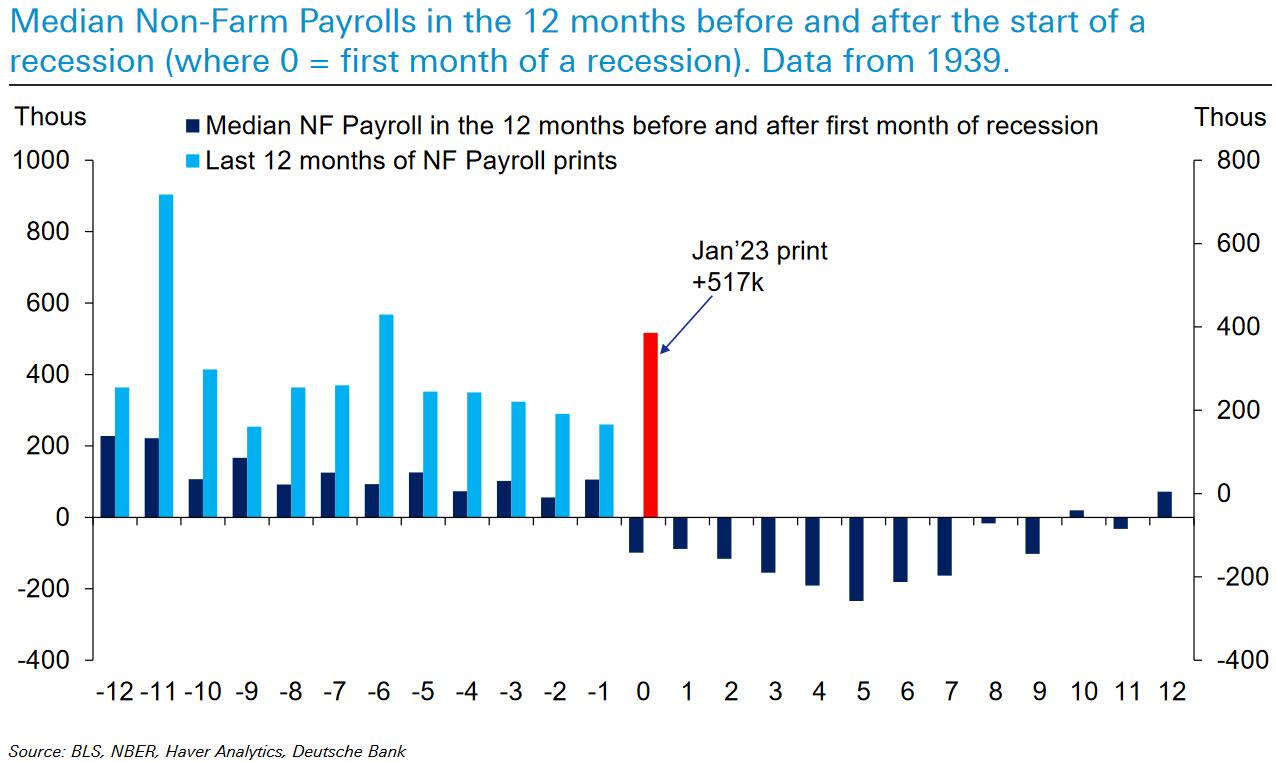

Deutsche Bank’s Jim Reid provided clients with some historical perspective on jobs data in relation to recessions. Jobs reports tend to weaken in the 12 months heading into a recession. Assuming that a recession began in January, that would make January’s print unprecedentedly strong. It could be argued that US labor is well overdue for a negative print.

The other argument that can be made with Reid’s chart is that the US will avoid a recession entirely. Sadly, that doesn’t seem likely given the myriad of other recession signals markets have witnessed in recent months.

And so, while tomorrow’s jobs report will undoubtedly cause a major reaction from stocks, it’s also anybody’s guess as to what the headline jobs number will actually be. That should only amplify tomorrow’s move – up or down – while Fed officials ponder whether to uncork a 50 basis point rate hike at the next FOMC meeting.

{kind=link}