Rejoice swept through the trading floor on Friday as investors celebrated a potent job report and the crucial passing of a debt ceiling bill that saved the U.S. from a looming default. The Dow Jones Industrial Average flexed its muscles, leaping a staggering 610 points, equivalent to 1.8%. The S&P 500 and Nasdaq Composite followed suit, rising 1.4% and 1%, respectively.

The week concluded on a positive note for the major averages. The S&P 500 advanced by 1.7%, Nasdaq made strides of 2%, and the Dow, with the Friday surge, wrapped up the week 1.5% higher. The technology-laden Nasdaq appears on track to celebrate its sixth consecutive week of growth – a feat not achieved since 2020.

Nonfarm payrolls outperformed expectations in May, surging by 339,000 against the estimated 190,000 increase. This marked the 29th consecutive month of positive job growth. Although the robust employment data had earlier induced pressure on stocks due to potential Fed rate hikes, Friday brought some relief. The data indicated average hourly earnings climbed less than predicted year over year, while the unemployment rate exceeded forecasts.

Charlie Ripley, the Senior Investment Strategist at Allianz Investment Management, summed up the day’s trading sentiment: “There was a little bit of a flavor for everyone today. It’s kind of providing that mixed picture for the Fed.”

Rising unemployment, slowed wage growth, and a big payrolls beat. What’s not to love?

Sentiment was further buoyed by developments around the U.S. debt ceiling. The Senate passed a bill to raise the debt ceiling late Thursday night. The legislation now awaits President Biden’s signature. This move followed the House’s passage of the Fiscal Responsibility Act, which significantly eased market concerns over a potential U.S. default.

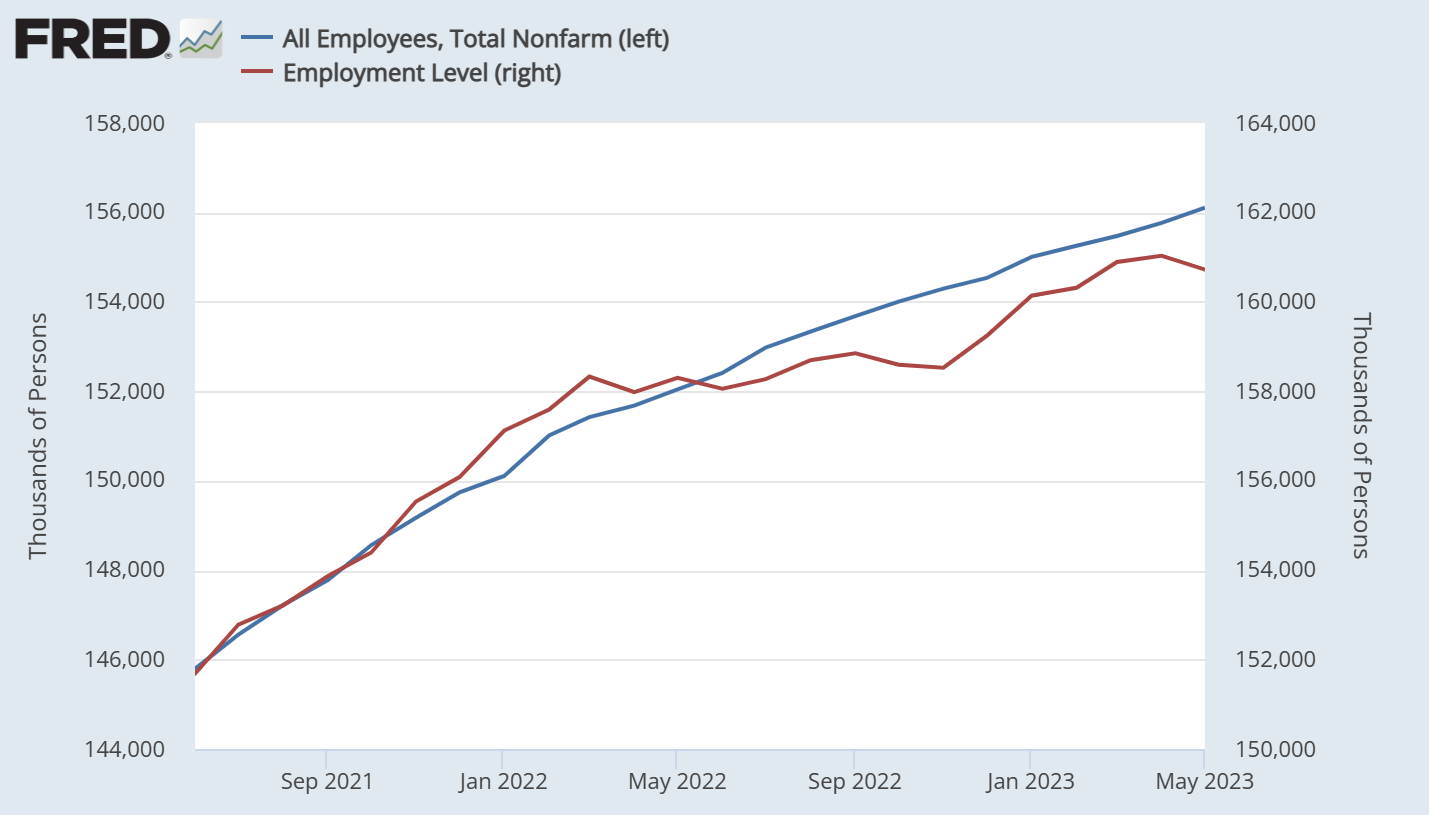

Despite this, Treasurys sold off today, likely in response to the strong headline jobs gain. But it was another confounding report in that workers fell by roughly 310,000 in May opposite payrolls (+339,000).

The gulf between payrolls (blue line) and workers (red line) is growing again as a result, likely due to the continued increase in multiple jobholders. Multiple jobholders were up 5.8% year-over-year last month following seasonal adjustments. The number of Americans holding multiple jobs popped in mid-2021 and has remained high ever since.

And though stocks blasted higher again in response to this data, Treasurys did not. Yes, unemployment went up, but was it enough to back the Fed off a June rate hike completely with inflation still well above the Fed’s target?

Probably not. According to JPMorgan cash trader Matt Reiner, today’s rally was driven by FOMO bulls:

“Flow compositions are shifting around the edges, and it all leads to performance chasing. But I think the most notable thing is no one is selling in size… Trimming, yes. Shorting, barely. Exiting winning positions, absolutely not.”

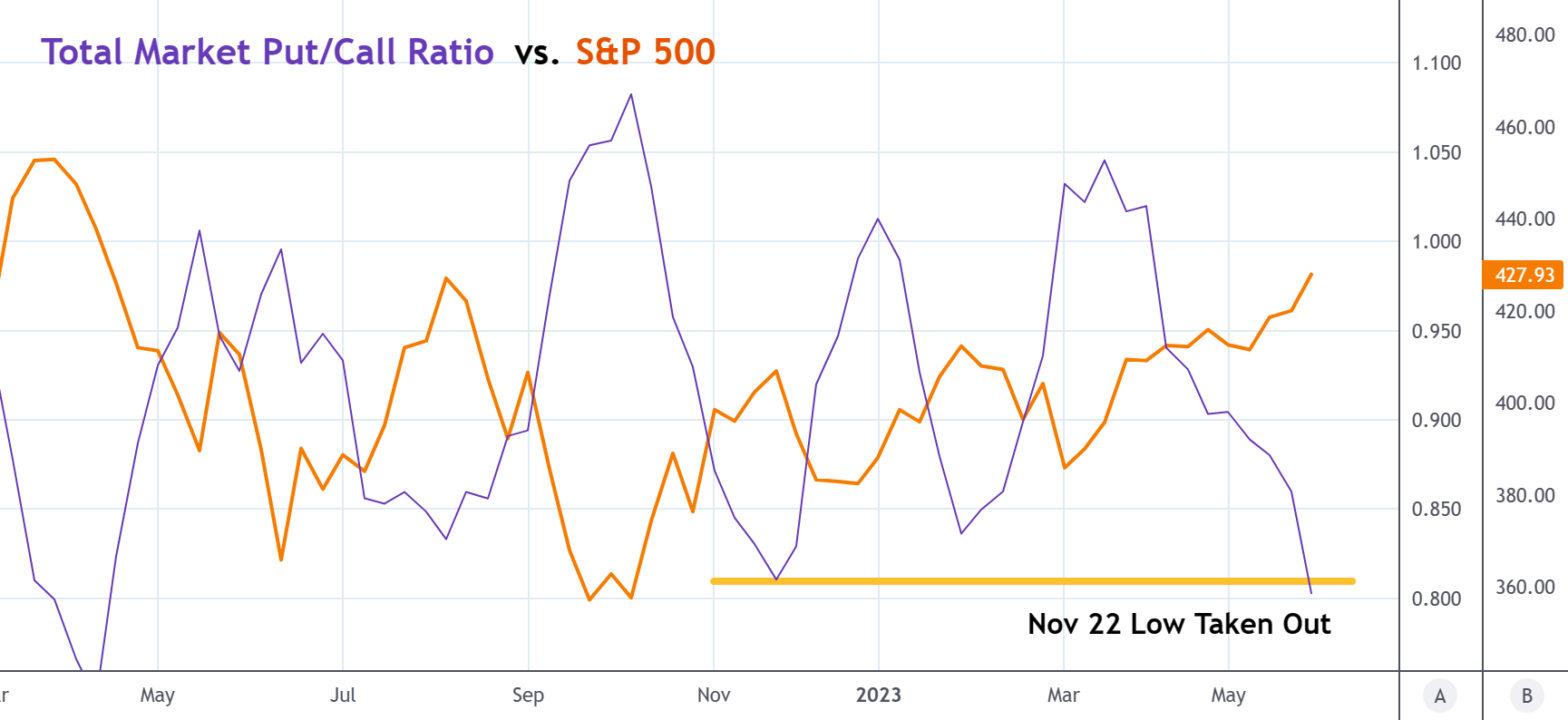

The “chasing” will eventually end, however, and that might happen soon according to the total market put/call ratio (PCR) as of this morning:

The PCR (with a 5-week moving average applied to it) just took out its November 2022 low. When the PCR bottoms, S&P selloffs always follow. It’s not clear exactly when the PCR will bottom, but given its rapid decline, it should happen either this week or the next. It wouldn’t surprise me at all to see this happen in response to new hawkish remarks from Fed officials ahead of the June FOMC.

So, while the going may still be good following today’s jobs report, it seems that the end is nigh; some bulls will start to realize that, which should flip the PCR higher as stocks finally come back down to earth.

{kind=link}