Stocks ticked slightly higher today as Wall Street attempted to recover from a week of losses. This upturn coincided with investors gearing up for key US inflation data later in the week, and the kick-off of second-quarter earnings.

The Dow jumped 0.4% while the S&P enjoyed a marginal gain of less than 0.1%. The Nasdaq Composite faded by 0.2%.

The Consumer Price Index (CPI), slated for release this Wednesday morning, will be followed by the Producer Price Index (PPI) on Thursday. These data releases follow last week’s jobs report which fueled concerns about additional rate hikes this year.

The previous week saw the S&P fall by 1.16%, splitting the difference between losses from Nasdaq Composite (-0.92%) and Dow (-1.96%). Even though June’s nonfarm payroll growth fell short of expectations, hotter-than-anticipated wage growth ultimately applied bearish pressure to markets.

Despite this, perma-bull and Fundstrat founder Tom Lee believes that investors are about to be treated to a cool CPI reading, potentially igniting a rally through the rest of the month.

“We thought a tactical sort of opportunity was emerging because last week the market sold off because the jobs report was too strong, yields really popped,” he said.

“So investors are kind of [fearing] Fed higher for longer [and are a] little bearish into this week, and I think core CPI could come in at [+0.2% MoM] or better.”

The market also has to navigate through a wave of quarterly earnings reports this week. Financial heavyweights such as BlackRock, JPMorgan Chase, Wells Fargo, and Citigroup will set the pace for the Q2 earnings season.

Bank shares were up this morning in anticipation.

But not all is well; according to Bank of America’s high-yield credit team, Treasurys are indicating a coming crisis. The warning comes on the heels of interest rates reemerging as a significant factor last week.

More specifically, the 10-year Treasury jumped back over 4% for the first time since February, and the 2-year Treasury brushed against 5.12%, marking the highest level since June 2007. Over in the UK, the 10-year yield has pierced the 4.64% ceiling – the highest since gilts imploded last October in response to finance minister Kwasi Kwarteng’s poorly-received budget proposal.

The threat of fluctuating rates has resurfaced, taking center stage as the primary driver of volatility in credit. As the credit market oscillates, so follows the rest of the market, reinforcing the interconnectedness of these sectors.

Bank of America’s core perspective is that the full damage caused by the Fed’s rate hikes can only be fully assessed once rates have peaked. We’re evidently not at that just stage yet with an assumed 25 basis point increase on its way in a few weeks.

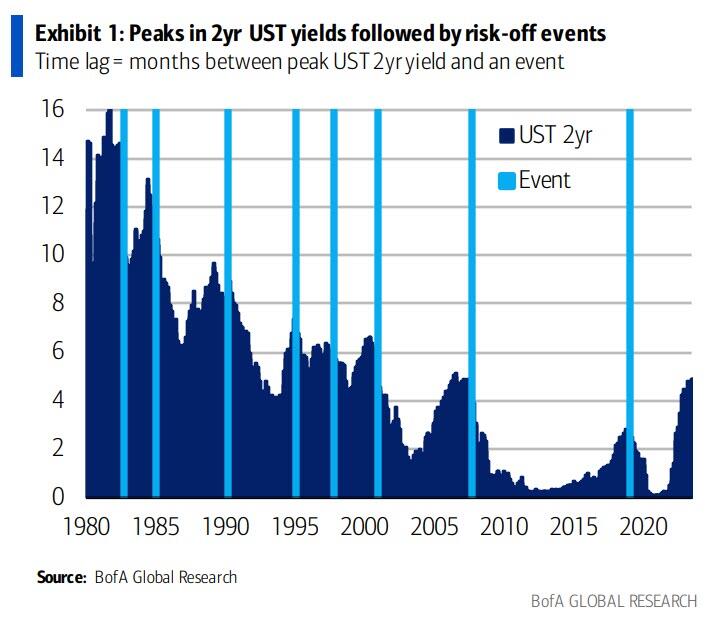

The bank’s analysts provided the chart above, which shows that every instance of a local peak in 2-year Treasury yields in the last 40 years has been followed by some sort of crisis. These events have varied in their impact from mild – such as the Mexican peso crisis in Dec 1995 (HY +95bp) – to moderate, like the Asia FX crisis in Oct 1997 (HY +350bp), to severe instances like the Global Financial Crisis (HY at all-time wides).

The delay between the peak in 2-year yields and the subsequent crisis has ranged from a couple of weeks to just over a year, averaging at seven months. The million-dollar question now is: how significant an ‘event’ could we potentially face this time?

To appreciate the magnitude of challenges ahead, BofA clarifies that the total G20 non-financial debt sits at $250 trillion, roughly twice its level since 2008. Bloomberg’s Global Agg yield, the broadest measure of fixed income, is currently at 4%, up from just under 1% in 2021.

Meanwhile, the average coupon on this index has only reset by +50bp. Most issuers continue to pay the old coupon and are yet to bear the full brunt of higher rates. Hypothetically, if all coupons were to reset by +320bp to match the change in yield, the cumulative interest expense of all G20 borrowers could skyrocket by $8 trillion.

That’s a big number, and just about the combined GDP of Japan and Germany, the third and fourth-largest economies in the world.

This is likely not an imminent threat, especially with at least one more rate hike on the docket. But, it should provide traders with some confidence that when 2-year Treausrys finally do peak, it’s only a matter of time – on average, 7 months – until another crisis hits.

{kind=link}