Stocks erupted higher today as bailout optimism hit a fever pitch. The Dow, S&P, and Nasdaq Composite all soared, setting new session highs with each passing hour. Bank stocks led the way as First Republic Bank (NYSE: FRC) jumped over 50% through noon.

It was a strong relief rally, but will those gains hold? Bleakley Financial Group CIO Peter Boockvar remains skeptical.

“Considering how much they’ve gotten destroyed, they’re due for a bounce back,” Boockvar said.

“The challenge for banks, in my opinion, is more of what the profit outlook is rather than viability.”

The February Consumer Price Index (CPI), which normally controls the trading session following its release, came out this morning, revealing that inflation rose by 0.4% month-over-month (MoM) and 6.0% year-over-year (YoY). Core gained 0.5% MoM and 5.5% YoY. Both headline and core met estimates. Shelter inflation dominated the report, accounting for roughly 70% of the core CPI gain.

It wasn’t the soft print that bulls were hoping for, but it also didn’t get in the way of the banking rally. Will it prompt a rate hike pause at the next FOMC meeting, though? Bloomberg economist Anna Wong weighed in:

“On a 1-month, 3-month, or 6-month annualized basis — metrics that Fed officials use to gauge inflation momentum — February’s headline CPI was running at 4.5%, 4.2%, 4.3%, respectively, with the two longer measures up from the previous month,” Wong wrote.

“On the other hand, core was up across the board: at 5.6%, 5.2%, 5.1%, respectively. The robust core CPI print is bad news for the Fed’s preferred PCE gauge. The 12-month change in core PCE inflation may accelerate to 4.8% from 4.7% for February, both far above the 2% target. That’s the opposite direction of where the Fed wants to it to be moving.”

Boockvar commented on the CPI as well in a note to clients.

“We have again a further acceleration in service prices that is offsetting the continued moderation in goods prices. That said, we know rental growth is being way overstated but should still grow 3-4% sustainably after the current supply increase gets absorbed as the demand is still very solid,” explained Boockvar.

“Goods prices on the other hand have likely bottomed on the downside of the spike. The combination is still going to lead to slower but sustainable inflation and why the Fed is going to hike rates by 25 bps next week but likely pause thereafter. The call for a rate cut next week by a particular bank makes no sense to me as the Fed would look so weak in doing so and would make all the vocal hawks look silly.”

Despite calls from Goldman for a rate hike pause (and even a cut from Nomura analysts), Boockvar’s probably right. The Fed will raise rates again before taking a serious look at halting hikes as recession signals emerge. A very weak March jobs report print, for example, could keep rates level in April.

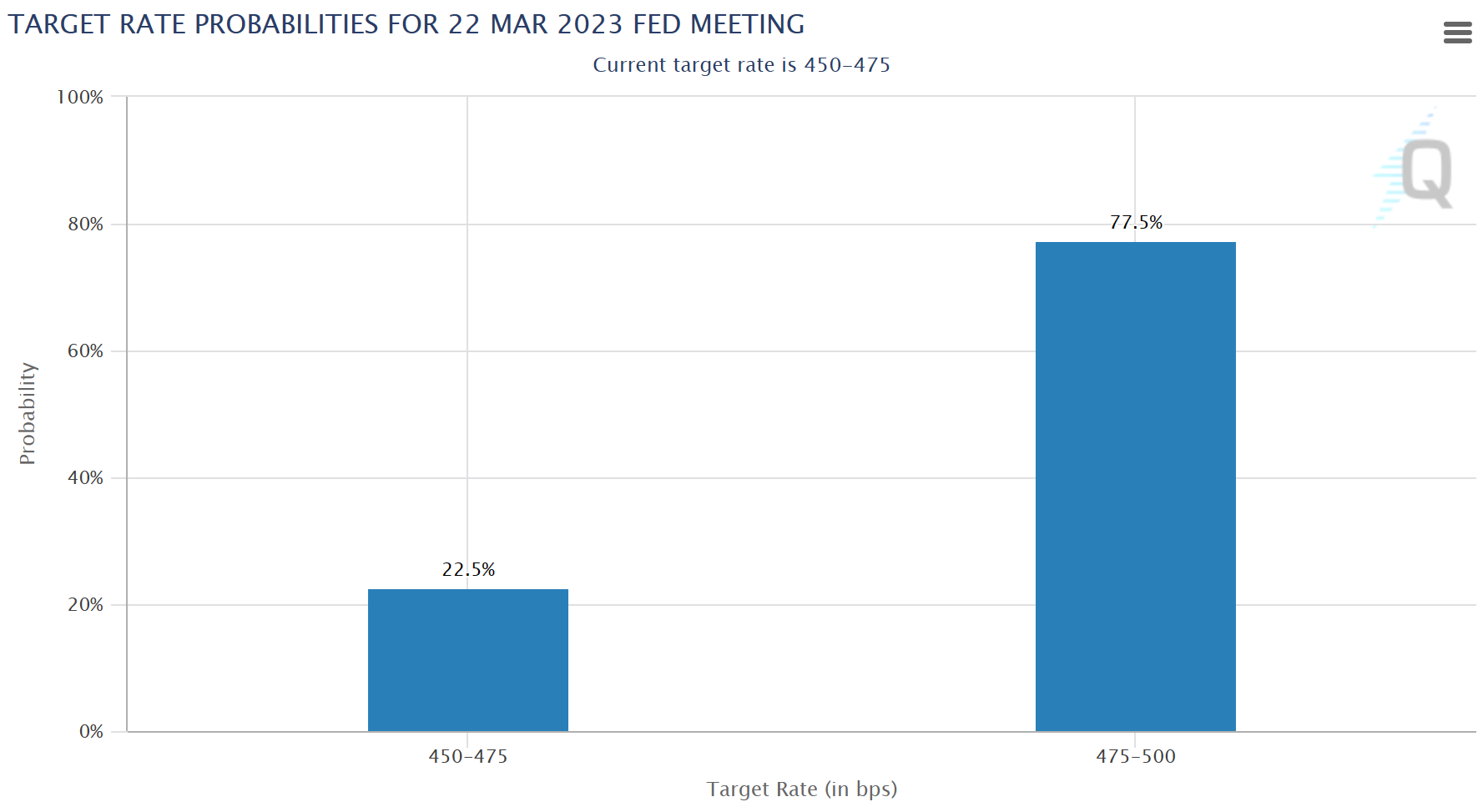

But the market might still be happy with a 25 basis point hike at the next FOMC meeting based on the most recent rate probability reading from the CME Group.

The market is currently pricing in a 77.5% chance that the Fed raises rates by 25 basis points this month. This is a stark contrast from just one week ago when the market saw a 69.2% chance that the Fed would hike by 50 basis points.

Independent of the bank bailout, that’s a big part of why stocks are rallying.

Is the selloff over, though? Probably not; it will take some heavy lifting from bulls to flip the market’s short-term trend. And until investors can string together a few more positive days, today’s gain feels much more like a “sell the peak” moment than anything else.

{kind=link}