Stocks fell today following a hotter-than-expected Producer Price Index (PPI) reading, released this morning. The Dow, S&P, and Nasdaq Composite opened significantly lower before rallying intraday to pare back their losses. Producer inflation jumped by 0.7% month-over-month (vs. 0.4% expected) and 6.0% year-over-year.

“Both inflation readings this week point to the stickiness of inflation and that the fight isn’t over, especially when considering today’s PPI reading was the highest month-over-month increase since early summer,” said Morgan Stanley portfolio construction chief Mike Loewengart.

“It shouldn’t be a surprise to see the market take a breather as hopes of a dovish Fed in the coming months fade. Bottom line is investors should recognize inflation may not return to normal levels as quick as many hope, and with that may come more volatility.”

Today’s PPI was a big “beat” that initially drove futures lower before Cleveland Fed President Loretta Mester applied additional bearish pressure.

“At this juncture, the incoming data have not changed my view that we will need to bring the fed funds rate above 5% and hold it there for some time,” said Mester at an event this morning.

“Indeed, at our meeting two weeks ago, setting aside what financial market participants expected us to do, I saw a compelling economic case for a 50 basis-point increase, which would have brought the top of the target range to 5%.”

The market had assumed that the Fed would use a series of 25 basis point increases to bring the fed funds rate to 5.0%, the Fed’s current target. A 50 basis point increase would not only double the Fed’s anticipated pace of increases but open the door to a higher terminal rate as well.

“Over-tightening also has costs, but if inflation begins to move down faster than anticipated, we can react appropriately,” Mester concluded.

Mester is not a voting FOMC member at the moment, but she soon will be if Chicago Fed president Austan Goolsbee is appointed to Fed Vice Chair, replacing current Vice Chair Lael Brainard who is on her way out to work at the White House. When Brainard leaves, Goolsbee will serve as the interim Vice Chair and Mester will fill his current position, giving her temporary voting rights until a more permanent replacement is found for Goolsbee. At that point, Gooslbee will step back down, taking his vote back from Mester who will be rotated out once more.

It’s complicated, but when Brainard steps down, that means the Fed’s biggest dove (Brainard) will no longer have a vote. Mega-hawk Mester will be voting instead, and at a time when the Fed is considering whether to raise the target rate above 5.0%.

Keep in mind that Goolsbee is by no means a shoo-in; he’s being considered among several other candidates. But his appointment to the position could have huge ramifications for traders as the Fed loses a dove and gains a hawk at a critical moment.

Mester’s comments (and the fact that she could potentially be a voting FOMC member soon) caused stocks to open significantly lower. But wild intraday dip-buying slashed the market’s losses through noon.

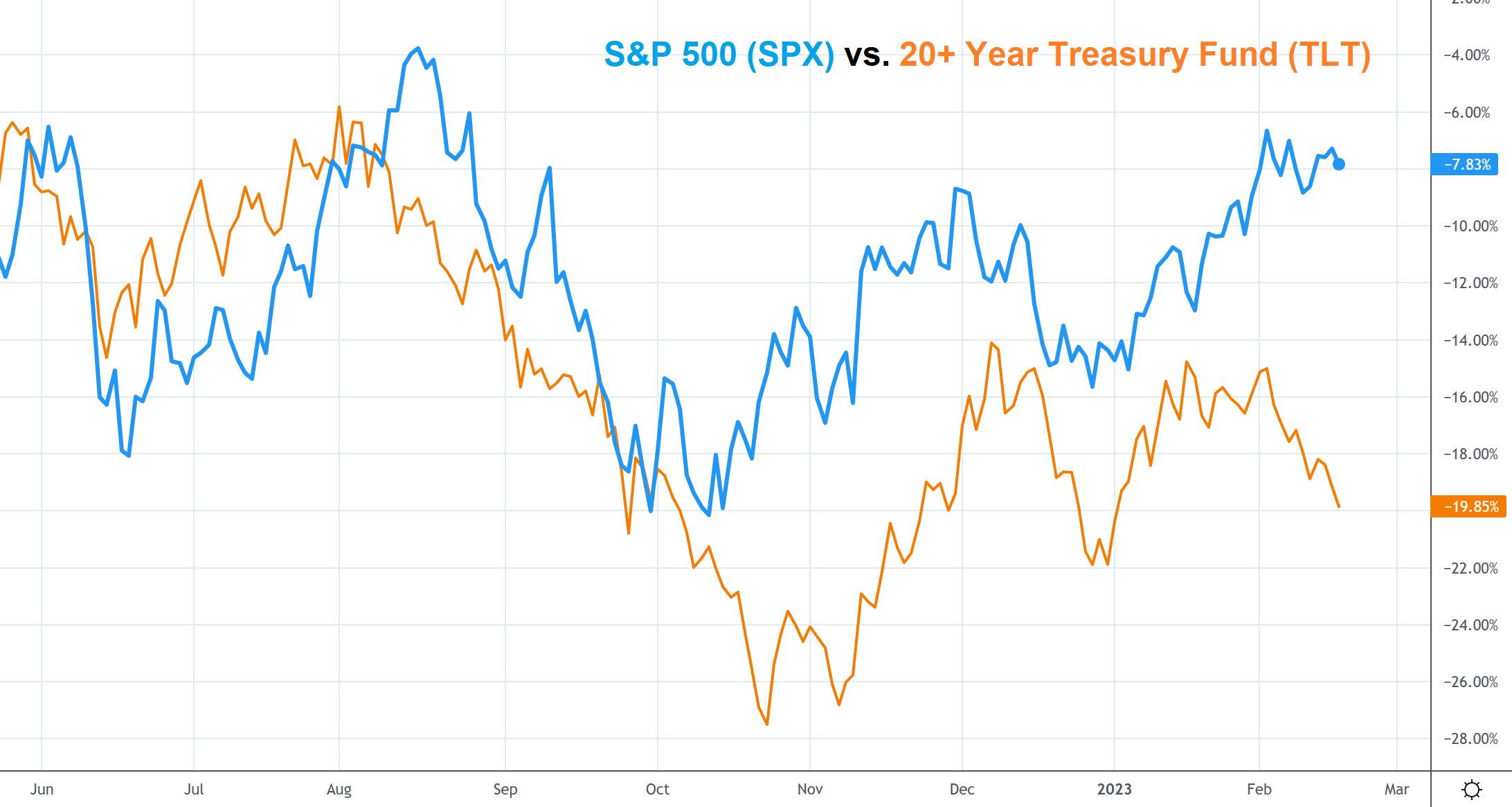

Treasury yields continued climbing as well. Treasurys and stocks have moved in tandem over the last year and a half. Over the last few weeks, though, that relationship started to break down.

Stocks are up but Treasurys are down sharply. Tech has even outperformed the general market despite rising yields. This kind of thing shouldn’t happen. Or, at least, it didn’t use to happen.

But a buying frenzy fueled almost entirely by retail traders drove Wall Street to cover its tech shorts. Covering then turned into outright chasing from hedge funds according to Goldman Sachs analyst Vincent Lin.

“Hedge funds are once again re-risking and have net bought US Info Tech for 11 straight days, led by long buys in the past week,” Lin wrote yesterday.

This behavior won’t last forever, and when the market eventually sobers up, the gap between Treasurys and stocks should narrow quickly as the S&P joins long-term Treasurys in their recent sell-off.

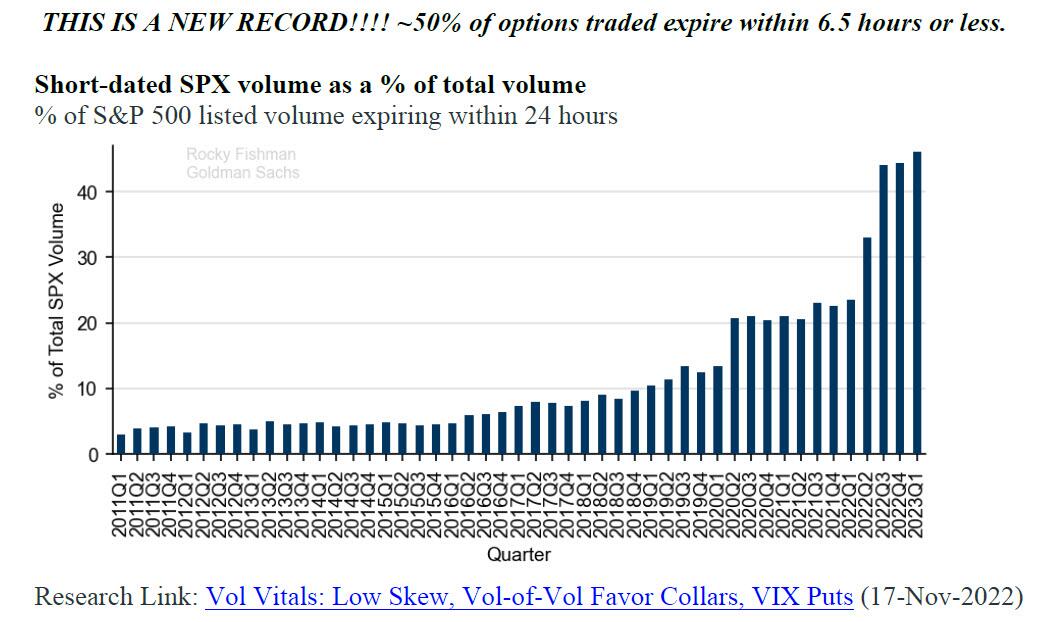

However, in order to catch up to Treasurys, stocks will need to move lower rapidly. A massive increase in zero days to expiration (0DTE) options trading activity could provide the volatility required to make this happen.

A recent Goldman Sachs note from strategist Rocky Fishman showed just how popular short-dated S&P options have become over the last two quarters.

Simply put, the market is very unstable right now as a result of 0DTE options and tech-chasing hedge funds are scrambling to eke out some last-minute gains after eating major short-squeeze losses. When hedge funds hit their limit, the resulting selloff could be violent as stocks race lower to meet Treasurys, likely via a series of 0DTE-driven intraday plunges.

{kind=link}