Stocks surged this morning as bulls quickly erased yesterday’s big loss. The Dow, S&P, and Nasdaq Composite all traded significantly higher shortly before noon, with Dow industrials leading the way. Traders have had to contend with an indecisive market for weeks, now.

Fundstrat’s head of research, Tom Lee, believes the instability may finally be ending.

“Our central case has been for a choppy July” explained Lee.

“While this is a possibility, we think there is a chance [Thursday] marked the peak of [the] ‘growth scare’ and if this is correct, equities might be shifting towards a broader risk on.”

Other analysts see a correction on the horizon.

“The market is solidly mid-cycle and with that typically comes a 10-15% index level correction. We expect such a correction will create buying opportunities given a still strong growth backdrop,” said Mike Wilson, Morgan Stanley’s chief U.S. equity strategist.

“Our economic growth forecasts remain positive, but bigger bulls continue to talk about ‘pent up demand’,” he added.

“We agree there is pent-up demand for services consumption. We also think the degree of overconsumption in goods and the ensuing payback is under-appreciated as the positive effects on income from stimulus checks and the surge in asset prices fade.”

Much of the reason for today’s snap-back recovery was a daily rise in Treasury yields. Yes, the market usually prefers its yields falling. But recently, a massive bond rally cast a pall over equities. This squashed long-term Treasury yields as 10-year and 30-year Treasurys quickly climbed.

The yield curve grew flatter as a result (and fast). That was bad for banks, which enjoy bigger lending margins with a steep yield curve – i.e., low short-term rates, high long-term rates.

Now, though, the gap between long-term and short-term yields has narrowed. This shrunk bank margins somewhat dramatically over the last week.

Today, Treasury yields jumped higher. But will they continue to go up? Or is this just a “dead cat bounce” prior to another bond eruption?

More importantly:

What’s driving this sudden shift in trends?

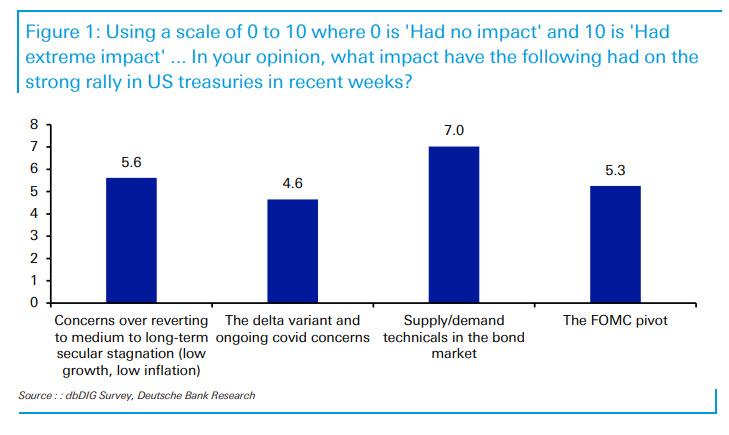

Deutsche Bank analysts found that Wall Street’s mostly split on the reasoning (technical vs. fundamental) for the rapid bond rally.

JP Morgan strategists, on the other hand, seem to be convinced that technical pressure is causing the “yield crunch.”

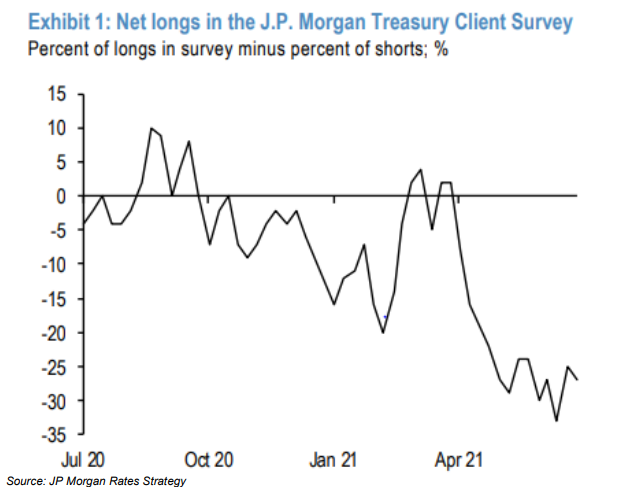

The JP Morgan Fund Managers Survey found that commodity trading advisors (CTAs) are massively short Treasurys. And as Treasurys went up in price, shorts were forced to cover their positions, driving bonds up even further. It’s a classic short squeeze, just like the ones that launched GameStop and AMC to epic melt-ups.

But the squeezing isn’t done just yet according to Morgan Stanley derivatives strategist Chris Metli, who said that CTAs still have to buy roughly $95 billion of Treasurys in notional value – the value of the underlying Treasurys in the short derivatives positions – over the next week.

Morgan Stanley noted that this “could continue the bond rally and put pressure on stocks as equity investors fear the bond market knows something they don’t about future growth prospects.”

Meanwhile, China just freed up 1 trillion yuan ($155 billion) by reducing bank reserve requirements in an attempt to support its slowing economy. Mass liquidity’s a popular solution to economic problems over there, too.

So, in both the East and the West, rate shake-ups are afoot. That should make the already volatile trading environment even more so as July draws to a wild, potentially explosive close a few weeks from now.

{kind=link}