Stocks traded flat through noon today after opening higher in response to the April Consumer Price Index (CPI), which was released before the market opened this morning. The Dow fell while the Nasdaq Composite advanced modestly. The S&P remained mostly unchanged from the session prior.

Inflation was slightly weaker than expected last month, leaving bulls and bears alike underwhelmed. Headline inflation advanced 4.9% year-over-year (YoY) vs. 5.0% expected while core CPI, which excludes food and energy, rose 5.5% YoY as estimated. Both core and headline CPI fell 0.1% from March’s annualized numbers (+5.6% for core, +5.0% for headline in March).

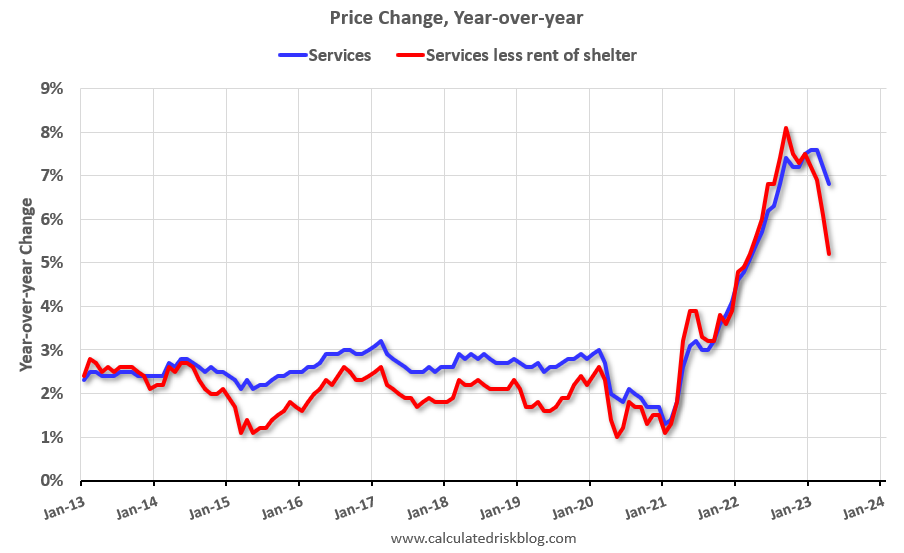

Core services excluding shelter, the Fed’s favorite new inflation metric, abated significantly as well, rising just 5.2% YoY compared to March’s annualized gain of 6.1%.

This should have excited bulls far more than the slight headline CPI “beat.” And it seemed to at first, as S&P futures raced higher before trading opened.

But the Fed’s inflation target of 2% remains very far off, and unless services inflation continues to nosedive (or a banking meltdown ensues), the market probably still has a long way to go before the Fed starts slashing rates.

“Optimism for the disinflation process to remain in place is high as this report showed shelter prices remain elevated, which just means the lag we are seeing with rent prices should start [to] meaningfully show over the few months,” said Oanda strategist Edward Moya.

“Inflation should continue to decline over the next few months, but falling back to 2% will be a lot harder given the strength in the labor market.”

While we may disagree with Moya’s appraisal of US labor, he’s right in that the Fed will have a difficult time bringing inflation substantially lower. The easiest path to victory would involve a grim recession, and many critics believe that the Fed is about to cause one, intentionally or otherwise. This is something that bond king Jeff Gundlach has repeatedly touched on in interviews over the last year.

More recently, though, Gundlach began mentioning how high rates are jeopardizing regional banks, and that it may only be a matter of time until another small bank goes belly up.

“Leaving rates this high is going to continue this stress,” Gundlach said last week after California bank PacWest toyed with the idea of a sale.

“I believe with a very high degree of probability there [are] going to be further regional bank failures.”

If that happens, the coming economic slowdown could be far worse than the Fed anticipates.

New York Fed President John Williams added to hawkish (and regional bank) fears yesterday when he said that inflation is still “too high.” This comment, among others, was made prior to this morning’s CPI release.

But JPMorgan analysts don’t expect a huge tone shift from the Fed any time soon.

“Recent Fedspeak [..] remains hawkish despite the Fed’s data dependent approach,” read a note to clients.

And that’s true; Fed Chairman Jerome Powell himself said last week that a recession is “unlikely.” Until some truly recessionary data comes in or a bank blows up, Powell will stay the course on rates, making the market’s short-term upside very limited.

{kind=link}