Stocks fell slightly today as tech led the market lower. The Dow traded flat while the S&P endured a small loss. The Nasdaq Composite underperformed, falling modestly, as yields rebounded. Regional banks sunk again, too, albeit far less than yesterday.

In general, it was a sleepy morning session that frustrated bulls and bears alike.

“None of the sectors are making convincing moves in either direction, reflecting a general lack of conviction in the market,” remarked Calamos Investments portfolio manager Joe Cusick.

He’s right in that index traders have been left sitting on their thumbs over the last week, but opportunities abound elsewhere; gold miners, banks, and oil stocks have done quite well for bears. Big Tech bulls probably feel quite happy as of this morning also.

For the broader market indexes, however, a disconnected market has kept things moving decidedly sideways. That’s reflected in the market’s extremely narrow market breadth, which grows narrower by the day.

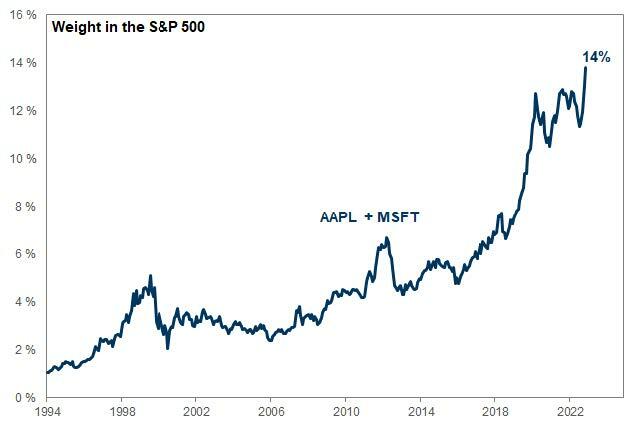

Combined, Apple (NASDAQ: AAPL) and Microsoft (NASDAQ: MSFT) now account for a massive 14% of the S&P 500’s total market cap according to a note from Goldman Sachs last week. Profits and profit margins are significantly higher among mega-cap names as well.

The market is splitting into the “haves” and “have nots.” And there are very few stocks that could be lumped into the former. The last time we saw breadth this narrow was back in late 2021, prior to the bear market of 2022. There’s not just a longer-term drawdown to be afraid of, though. Narrow breadth also lends itself to sharp selloffs.

We haven’t had a limit down day since Covid hit. It would not be all that surprising to see another one soon given how slim breadth currently is and the state of regional banking.

Slumping consumer sentiment could impact stocks, too. The University of Michigan’s Consumer Sentiment Index came out today, revealing a print of just 57.7 for May. That’s down roughly 6 points from 63.5 in April.

But perhaps the most notable portion of the report was its long-term inflation expectation reading, which climbed to 3.2%, hitting a 12-year high.

“Consumer sentiment tumbled 9% amid renewed concerns about the trajectory of the economy, erasing over half of the gains achieved after the all-time historic low from last June,” said Joanne Hsu, the survey’s director.

“While current incoming macroeconomic data show no sign of recession, consumers’ worries about the economy escalated in May alongside the proliferation of negative news about the economy, including the debt crisis standoff.”

She continued, adding:

“Throughout the current inflationary episode, consumers have shown resilience under strong labor markets, but their anticipation of a recession will lead them to pull back when signs of weakness emerge. If policymakers fail to resolve the debt ceiling crisis, these dismal views over the economy will exacerbate the dire economic consequences of default.”

The report unsurprisingly pulled stocks lower intraday after it was released. Will the S&P head significantly lower still, though? Not until Big Tech sags, which seems at least a few sessions away at the earliest should yields continue to rise.

{kind=link}