Stocks rebounded today in response to a cooler-than-expected March Producer Price Index (PPI) as Big Tech soared. The Dow, S&P, and Nasdaq Composite all ripped higher through noon, rising off their opening lows.

Producer prices posted a major “miss,” falling 0.5% month-over-month (MoM) in March vs. +0.0% expected. Even core prices, which exclude food and energy, dropped 0.1% MoM vs. +0.2% expected.

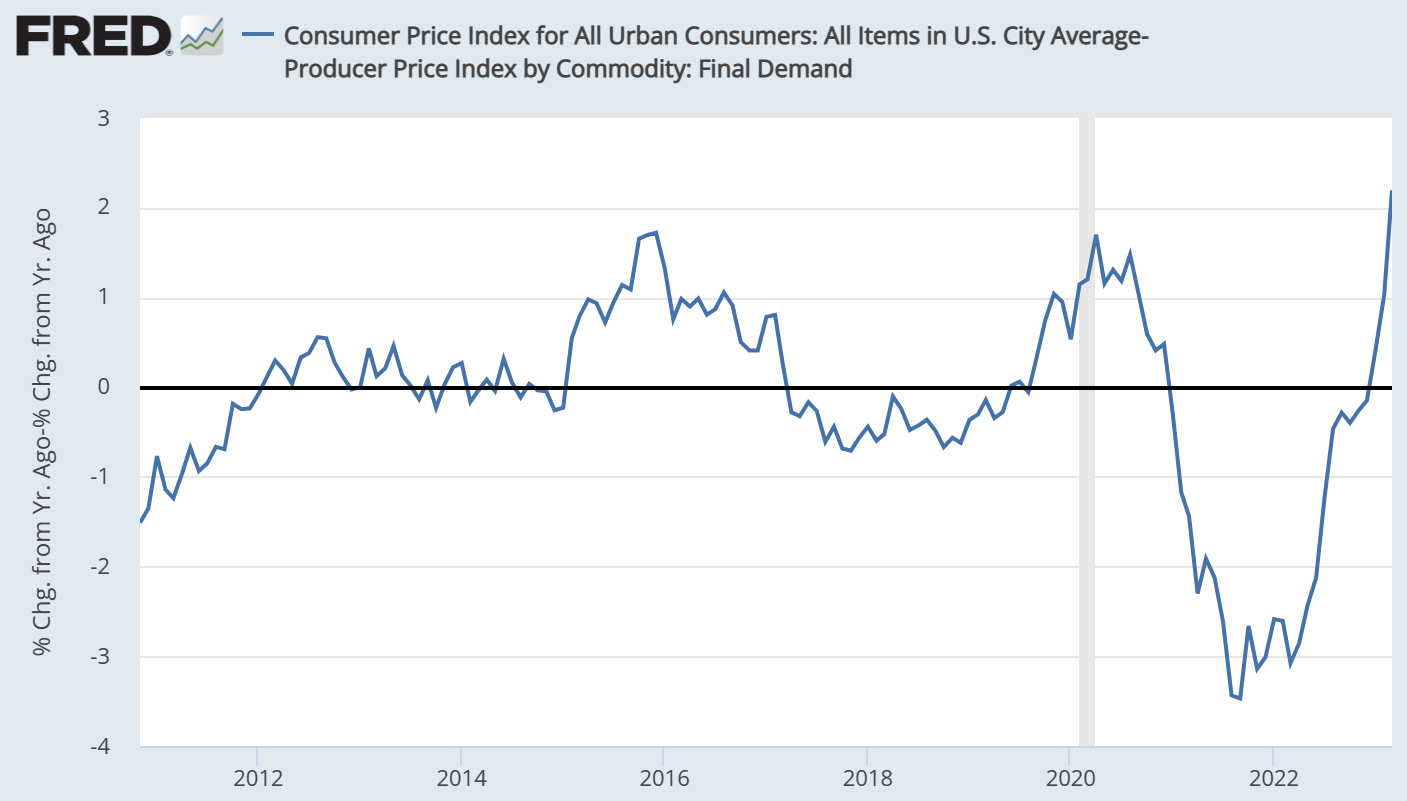

This was, by all accounts, a significant bullish surprise. And because PPI is viewed by many analysts as a leading indicator of CPI, it stirred up hopes of falling consumer prices in the months ahead.

“The market was a little poised to potentially go up on any positive news, and in this case, the PPI number was quite a bit better than expected. And I think that gives people some comfort that in fact the Fed probably doesn’t have to raise rates in the next meeting,” said Spouting Rock Asset Management’s Rhys Williams.

Not everyone’s convinced that the Fed will hold off on a rate hike, though. The CME Group’s FedWatch Tool showed that Treasury markets were still pricing in a 65% chance of a 25 basis point rate hike in May even after today’s PPI release. That’s down from 70% in response to the March CPI, but still higher much higher than it was following the Silicon Valley Bank meltdown.

“Markets might be getting a little too ahead of themselves, as far as optimistic, that the Fed will be able to cut when the markets are pricing that in,” said Megan Horneman, CIO at Verdence Capital Advisors.

“I don’t think the Fed’s going to be able to do that. I think the Fed’s going to have to stay on hold for longer than people anticipate, and then maybe rate cuts next year, but I think they’re going to have to stay on hold because we still are in a very sticky inflation environment.”

If nothing else, the gulf between CPI and PPI suggests that margins have improved significantly for producers.

In fact, the spread between CPI and PPI reached a record high last month, indicating that profitability could improve for many companies this summer even if net revenues fall due to an oncoming freight train of a recession – something the Fed is clearly concerned about according to the March FOMC minutes, released yesterday.

“Given their assessment of the potential economic effects of the recent banking-sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years,” read the meeting summary.

The minutes didn’t offer all that much clarity on rates other than “recession = bad” and that the Fed will hike if it’s “appropriate.” Today’s PPI went a long way in calming equity market fears.

That being said, Treasurys aren’t buying it. Market activity still points to a hike in May (via the CME Group’s FedWatch Tool) and bond traders are probably right. The Fed would rather overdo it than undercook rates.

Tomorrow, the US retail sales report comes out, and, based on recent credit card data from major banks, it’s expected to be a bloodbath. Big bank earnings are due out, too, and they should only amplify the market’s recession anxiety if forward guidance looks rough, which it probably will.

{kind=link}