The S&P held steady on Wednesday as traders mulled over fresh remarks from Fed Chairman Jerome Powell about the future pace of monetary policy. The Dow fell around 0.2%, or 70 points. The S&P climbed a slight 0.04%, while the Nasdaq won a 0.49% gain.

Powell hinted at more tightening measures ahead, including the possibility of back-to-back interest rate hikes.

“We believe there’s more restriction coming,” he said.

“What’s really driving it […] is a very strong labor market.”

Powell added that he wouldn’t “take [raising rates] at consecutive meetings off the table,” and “there’s a significant possibility that there will be [an economic] downturn.”

He made these comments while on a panel with other top financial figures, including Bank of England Governor Andrew Bailey, European Central Bank President Christine Lagarde, and Bank of Japan Governor Kazuo Ueda. They were attending the European Central Bank Forum on Central Banking in Sintra, Portugal.

At the same time, chip stocks stumbled on news from The Wall Street Journal that the U.S. might slap new export restrictions on China. This caused Nvidia to drop, as well as the iShares Semiconductor ETF.

Despite this, the Nasdaq managed to move higher as traders went back to buying up tech stocks. Amazon moved up 1%, while Tesla jumped almost 3%. Netflix shares climbed more than 4%.

“We’re all taking in the comments from the big four central bankers,” said Kim Forrest from Bokeh Capital Partners. “And it feels like the market really wants to go higher, but the whole, ‘we need to have higher rates for longer’ message is kind of serving as today’s cap.”

Investors are readying themselves to wrap up the best first half for the Nasdaq in 40 years. They’ve been riding a wave of optimism around artificial intelligence, which has significantly boosted a few mega-cap tech stocks. This year, the S&P and Nasdaq have risen about 14% and 30% respectively.

Some Wall Street strategists remain concerned about a continued selloff, however, following last week’s dip.

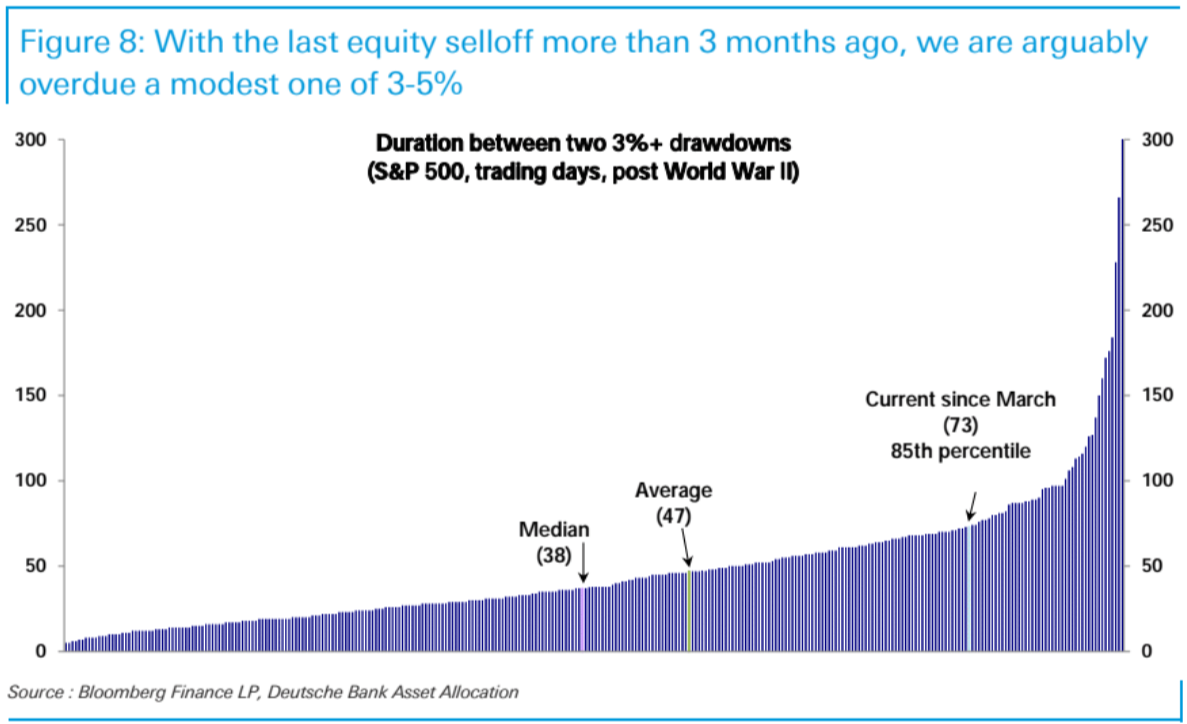

Yesterday, Deutsche Bank analysts predicted a 3-5% correction due to how long it has been since the last significant market drawdown (73 trading days).

JPMorgan analysts, on the other hand, feel more optimistic:

“The U.S. Market Intel view is that irrespective of price action over the next 3-4 trading sessions, stocks are poised to move higher, tactically,” read a morning note to clients.

“The combination of improving macro data, the end of the earnings recession, and line of sight into the end of the Fed’s hiking cycle will produce a tailwind. While there are likely to be liquidity constraints, induced by the TGA refill, that alone is not strong enough to derail this rally especially when considering the buyback bid that will return and the potential for private equity to drive a resurgence in M&A.”

In other words, JPMorgan is saying that stocks could still fall over the next few sessions but that won’t prevent a July rally continuation, even if stocks correct 3-5% (as Deutsche Bank predicts) prior to the rally.

The S&P was down from its recent peak by about 2.8% as of Monday’s close. Now, it’s only down roughly 1.5%.

Anything seems possible at this point, and a short-term selloff makes perfect sense. But ever since the debt ceiling debacle, stocks have behaved very erratically. Traders should expect the unexpected, even if that means rallying into yet another rate hike in July.

{kind=link}