It finally happened.

The 10-year/2-year Treasury yield curve inverted today, signaling to thousands (if not millions) of investors that a recession is coming.

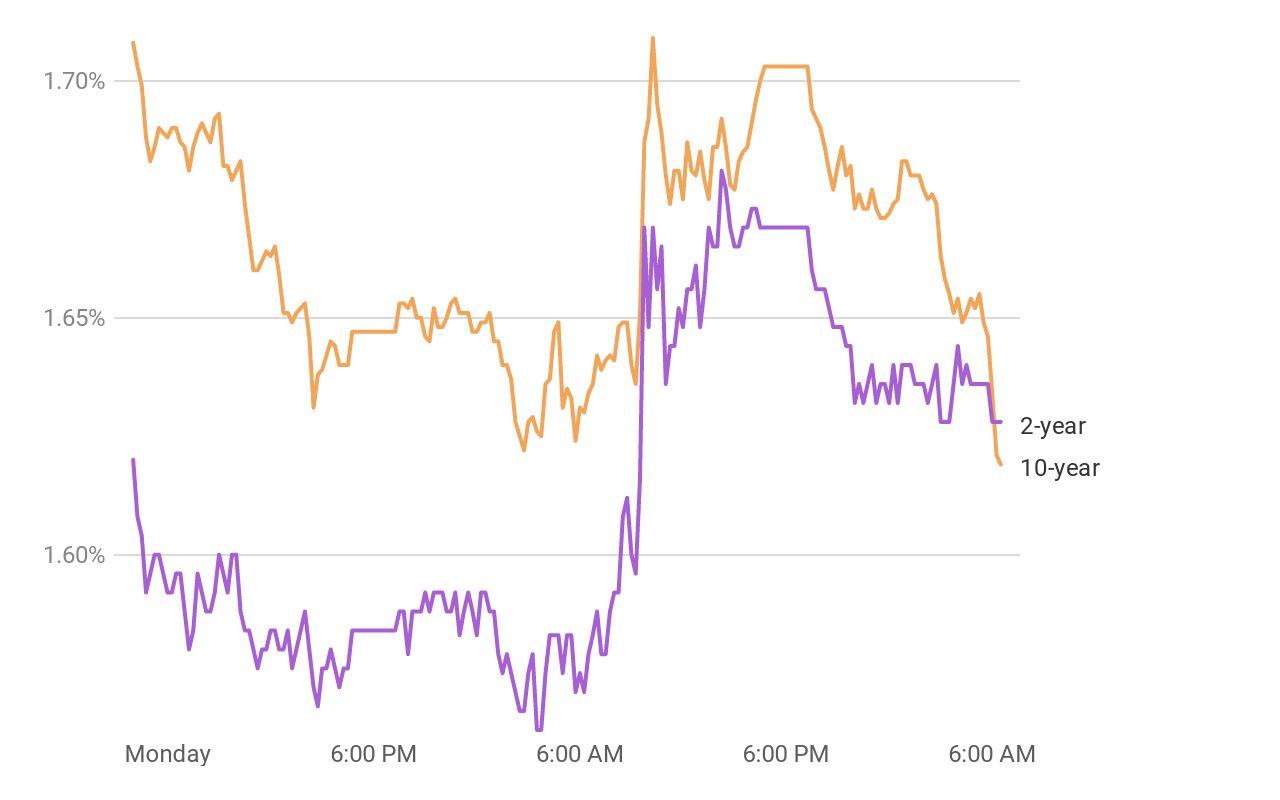

There were inversions in other short-term vs. long-term yield spreads over the past few weeks, like the 10-year/3-month, but none hold the same weight that the 10-year/2-year curve does. This morning, it fell temporarily to a negative 1 basis point for the first time since 2007.

And we all know what happened just one year later in 2008 – the financial crisis and a housing collapse.

It’s without a doubt one of the most nefarious indicators to analysts. After all, the last three inversions of the 10-year/2-year spread preceded economic calamity.

Today’s inversion, which comes weeks after the 10-year/3-month yield spread inverted (something we predicted), has Wall Street heading for the hills. Potentially for good reason, too, as recessions have historically arrived 18 months (on average) after the 10-year/2-year yield curve goes negative.

Many economists believe that this inversion is a good indicator of recessions because of its ability to reflect when strict monetary policy is limiting growth.

However, since 2008, the Fed has been more accommodating than ever before. Monetary policy is historically lenient and based on Fed Chairman Jerome Powell’s statements from his late July FOMC meeting, it could grow even more so.

Instead, what’s likely crunching bond yields is something else entirely. China is smack-dab in the middle of an economic slowdown – courtesy of the United States – and just recently posted its worst industrial production growth numbers since January 2002.

Germany’s economy actually shrank 0.1% in Q2 2019. Analysts place much of the blame on the U.S./China trade war, which they say continues to cause collateral damage in Europe.

They’re the kind of headlines that have investors certainly uncertain about nearly everything.

What they do know, however, is that short-term Treasury bonds shouldn’t generate higher yields than long-term ones. It theoretically doesn’t make any sense, and when government backed securities start to defy logic, it’s time to get worried.

And I don’t blame anyone who’s running scared after bond yield reports were released this morning.

But what investors need to be aware of is something I’ve repeated time and time again:

Yield curve inversions do not cause recessions. They are a symptom of something else.

In this case, the root cause of the 10-year/2-year inversion could simply be uncertainty over a prolonged trade war. Moreover, it might not be signaling a recession.

Don’t forget, the last three times the yield curve inverted (and recessions followed), the conditions were very different. Rates were high, and more importantly, the economy was soft.

These days, the economy looks somewhat healthy. Investors don’t seem to think so, but that doesn’t change the fact that the U.S. looks poised to continue growing at a steady pace.

That doesn’t mean the market won’t have its issues, though. We’re witnessing that as we speak.

But to suggest that another financial collapse is on the horizon simply because the yield curve inverted is a major over exaggeration of what’s really going on.

Trade war uncertainty, not inhibited economic growth, is driving treasury bonds in 2019. The sooner investors realize that, the better.

{kind=link}