The market’s tumbling this morning as Treasury yields rise. With the 10 Year Treasury Note falling, rates are up. That has investors concerned about how much longer the bull market can last.

The Dow’s flat on the day while the S&P and Nasdaq Composite trade for significant losses.

But it’s not just that yields are climbing. Investors seem uncomfortable with how fast they’re spiking as well. The 10Y yield is up 0.42% on the year.

And while that might not appear like a huge jump, keep in mind that the 10Y rate entered January at 0.93%. The leap to 1.30%+ marks an increase of roughly 40%.

That represents a major shift in Treasurys, as well as market psychology. The last time yields rose this quickly was in late 2018 when Fed Chairman Jerome Powell attempted to induce quantitative tightening.

The S&P corrected over 17% in response.

Will that happen again? It certainly could. Critics of the post-Covid, post-vaccine rallies continue to say that equities are overvalued.

If they’re right, and the 10Y yield enters the 1.40%-1.50% range, a vicious correction could follow. Wall Street analysts have observed that commodity trading advisors (CTAs) might be enticed to load up on short Treasury futures at around that level, eventually creating an avalanche of bearish pressure.

Which, in turn, would cause yields to break even higher, plunging stocks into a market-wide “crunch.”

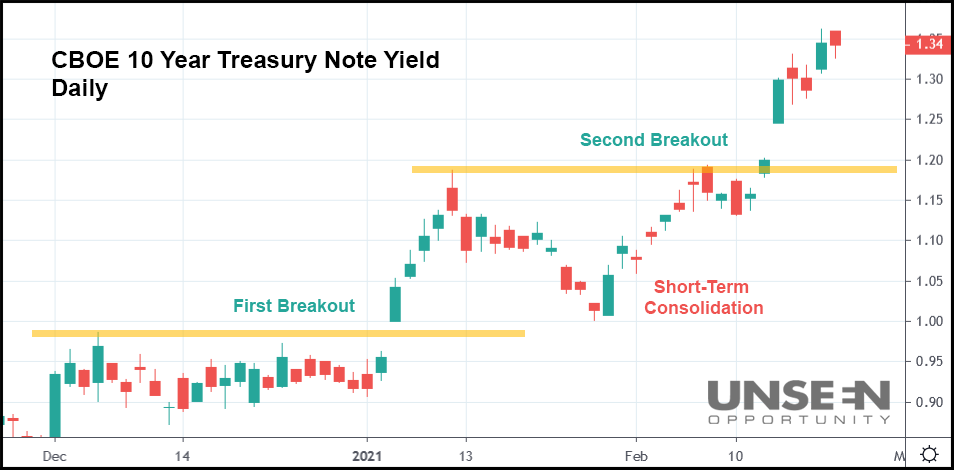

In the chart above, you can see that following the first 10Y yield breakout, a short-term consolidation phase preceded the second. We’re currently in that second breakout, and bulls are praying for yet another consolidation that sparks a yield downtrend, back to the 1.00%-1.20% range from earlier in the year.

It’s something analysts are taking note of now that stocks have begun stalling-out.

“This move in yields should be something that investors keep a close eye on,” explained Matt Maley, chief market strategist at Miller Tabak.

“Just because long-term rates are ultra-low on a historical basis, we do not believe that they will have to rise as far as most pundits think they do […] before they impact the stock market.”

Others refuse to budge, claiming that the ongoing torrent of stimulus and liquidity should keep bulls in the game.

“We do not see the recent increase in yields as a threat to the bull market,” said Keith Lerner, Truist’s chief market strategist, in a note.

“Given that we are in the early stages of an economic recovery, monetary and fiscal policy remains supportive, the sharp rebound in earnings, and favorable relative valuations, we maintain our overweight to equities.”

Tabak and Lerner both have valid points. Really, it’s all going to come down to timing. At what point will investors be unable to stomach higher yields? And at what level will “yield nausea” be reached?

These are both critical questions for the market’s short-term future as inflation worries weigh heavily on bulls. For certain sectors, their rallies could continue.

But the general market faces significant hurdles, now. So, in the coming days, watch to see where yields are headed. If the 10Y reaches 1.40%, it might be time to bail on stocks.

Simply because we have a market that has grown “fat” on low-yield expectations.