Covid cases are up. The market is down.

Does it feel like 2020 to anyone else?

The market opened for a big loss this morning, continuing last week’s trend as energy and industrial stocks led the way lower. Tech fell, too, albeit not nearly as much thanks to still-sinking long-term Treasury yields.

The 10-year Treasury yield momentarily dipped above 1.20% today before settling at 1.18% by the close. This flattened the yield curve further, thus crunching bank stocks. Banks prefer a steep yield curve to generate more profitable margins.

Conditions have only worsened over the last week in this regard despite strong bank stock earnings.

But more than anything else, a rebound in Covid infections had investors ready to sell. 30,000 new cases are being added per day in the US as the new delta variant of the virus spreads. Internationally, infections are up as well. And even among those who are fully vaccinated.

It’s not just Covid that’s providing sell pressure, though. Last Friday was July’s monthly option expiration date. And with a large number of contracts falling off the books, it was likely that a major move would result during today’s trading session. It just so happened to plunge the major indexes deeper into the red instead of helping equities break through to new highs.

“You have two concerns coming together this morning: concerns about market technicals and concerns about growth,” explained Mohamed El-Erian, chief economic adviser of Allianz and former CEO of PIMCO.

“That’s what all the asset classes are telling you this morning.”

But on the bullish end of the spectrum, technicals are also screaming “buy!”

The 50-day moving average (50-SMA) has been a very reliable technical trend-identifying indicator for the S&P 500 (as represented by the SPY in the chart above) in 2021. Each time contact was made with the 50-SMA, a rebound to a new high followed without fail.

Had investors bought the SPY the moment it touched the 50-SMA, they would’ve outperformed the index by a country mile.

The question is, however:

Why is this the case? Why are bulls buying every dip they come across?

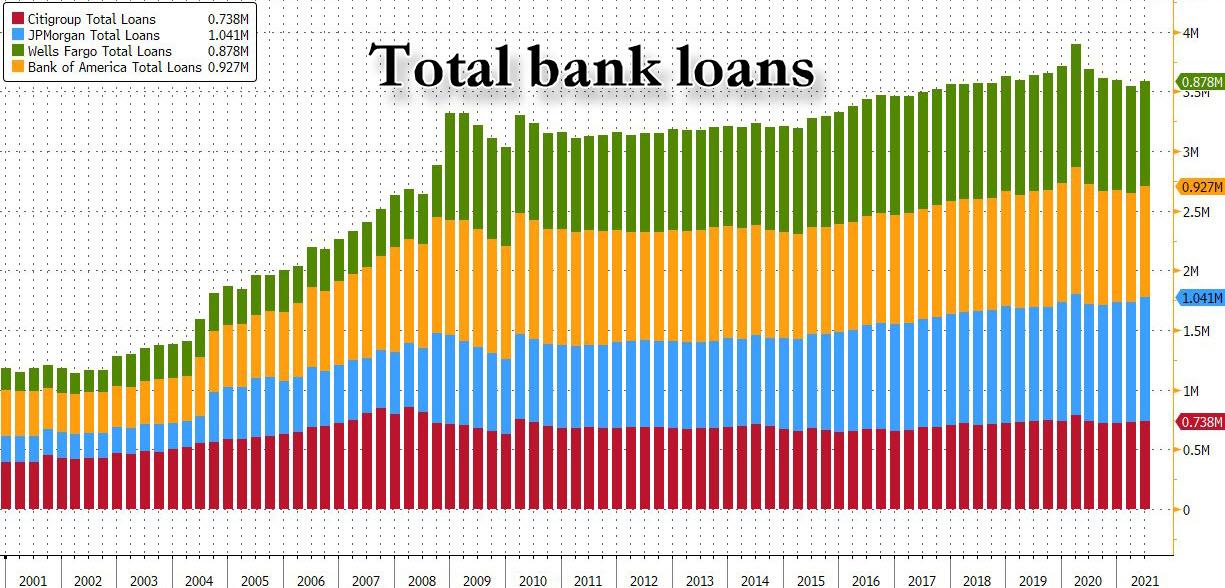

It all has to do with the Federal Reserve and quantitative easing (QE), which has effectively backstopped equities. Supporters of QE also subscribe to modern monetary theory (MMT), which states that loans drive deposits.

The idea is that by providing QE and keeping rates down, the number of loans would increase. These loans would then prompt economic growth, increasing the number of deposits held by banks.

This cycle would continue, expanding the economy under the guidance of QE and a watchful Fed.

But ever since 2009, when the Fed launched QE in response to the Financial Crisis, loans haven’t increased. In fact, Bank of America (NYSE: BAC) recently revealed in its Q2 earnings report that loans are actually down from where they were in 2009. The same is true for Citigroup (NYSE: C) and Wells Fargo (NYSE: WFC). Only JPMorgan (NYSE: JPM) has seen a net increase in loans over the last 12 years.

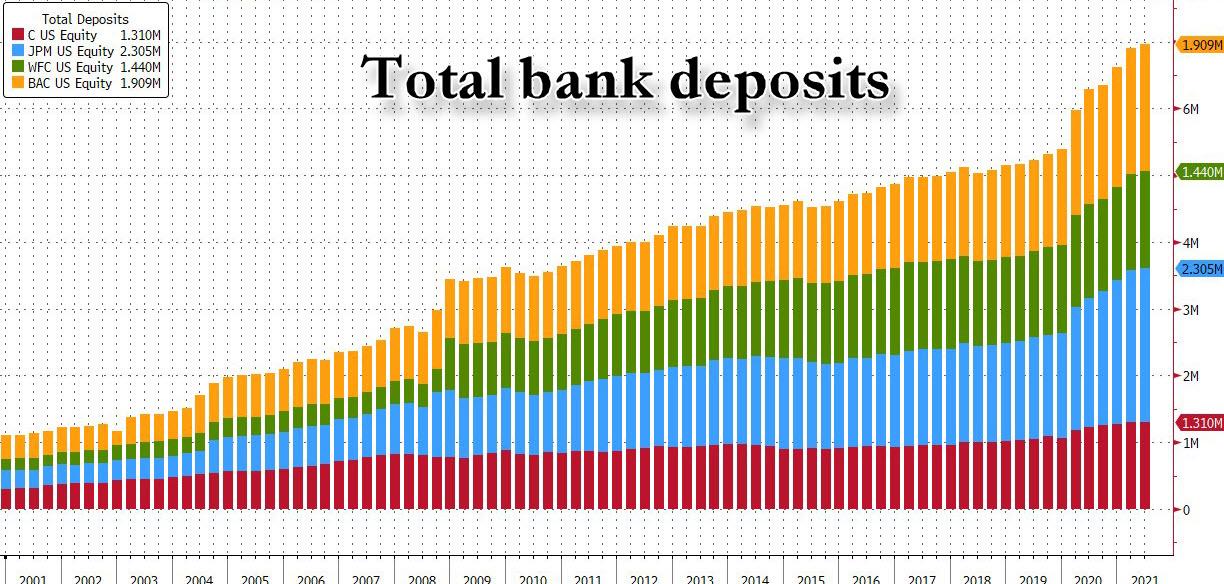

Meanwhile, deposits have soared.

This means QE has driven up deposits but not loans. Endless liquidity didn’t necessarily spur on economic growth as a result. It may have only contributed to asset bubbles in a major way, causing asset inflation (not just traditional price inflation) in the process.

So, what gives? Does this mean MMT is a false ideology?

It certainly appears that way. It is just a theory, after all. Economists remain split on whether it truly works.

That hasn’t stopped central bankers from applying it to the nth degree over the last decade, though.

The result has been a market that refuses to drop and banks that are artificially overstuffed with cash. They’ve turned to the repo markets in recent weeks to help soak some of it up.

But, as it turns out, much of that money likely worked its way into bonds and equities instead.

So, despite today’s selling, cashing out of stocks altogether could be a little premature. In fact, it may even be a good idea to double down and buy more.

Fed Chairman Jerome Powell said last week that the US economy has much further to go before the Fed even considers tapering QE. That could result in several more months’-worth of gains as Powell chases “full employment” (an unemployment rate of 3.5%). It’s a goal that he believes would signal a complete economic recovery.

However, the US may be entering a phase where it’s not even possible to attain that level of unemployment ever again. If so, this could keep QE running indefinitely.

Or, at the very least, until the next crisis comes along.

{kind=link}