Stocks plunged this morning while banks continued to reveal poor earnings. Bank of America (NYSE: BAC) reported a 45% decrease in first-quarter profits before the market opened, following JPMorgan’s (NYSE: JPM) equally disappointing numbers from Tuesday.

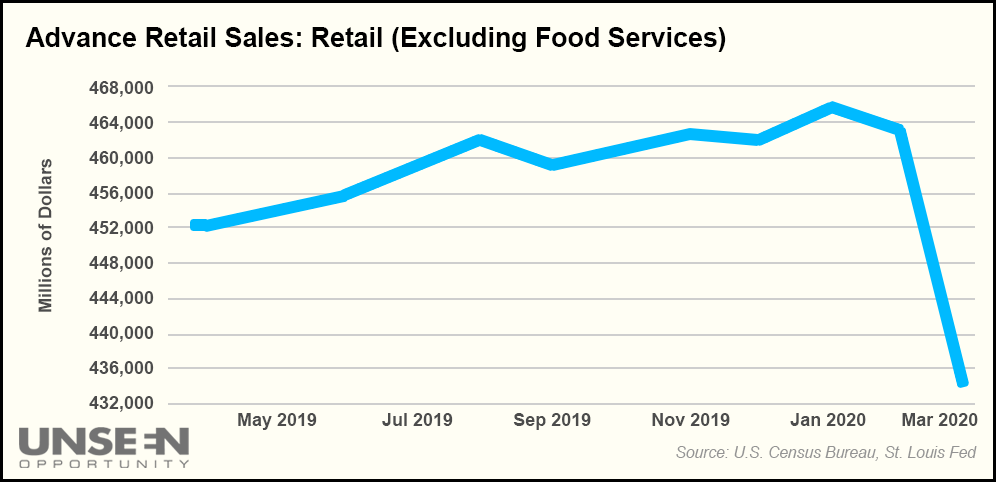

But the real story today is the Commerce Department’s newly released consumer and manufacturing statistics. In March, retail sales fell by 8.7%. That’s the biggest decline measured by the government ever. Meanwhile, New York regional manufacturing activity sunk an astonishing 78.2%.

Both numbers come by way of the COVID-19 crisis, meaning investors expected reduced productivity.

What they weren’t ready for, however, was the sheer magnitude of the retail and manufacturing losses.

Especially so early into the outbreak.

Analysts now predict even worse drops in April with 90% of the U.S. in “shutdown” mode.

“The economy is clearly in ruins here,” said Chris Rupkey, chief financial economist at MUFG Union Bank, in response to the reports.

“Nobody is buying cars, down 25.6%, nobody is buying furniture, down 26.8%, and eating and drinking places were down 26.5%.”

Rupkey continued, contrasting the current situation to the financial crisis:

“Retail sales in the fourth quarter of 2008 fell over 8%, but that was over three months,” he said.

“This was just one month […] Consumers are hunkering down at home, only venturing out to go to the grocery store. It’s lights out today, and as far as we can tell, it’s going to be worse next month.”

BMO senior Treasury strategist Jon Hill believes last month’s decline could even lead to a depression.

“It’s really going to be not only a function of infections declining and whether there’s a vaccine, but how will the economy be able to reopen and how quickly, given the depth of the hit to the labor market,” he said.

“These are very different types of recessions. One is broader economic impact. This is a sudden stop. It’s not surprising that things are economically skewed, but we’re not playing by typical economic rules. We’re playing by health policy rules. It’s going to be hard for [Treasury] rates to sell off in any meaningful fashion.”

And in his commentary, Hill highlights the crux of the issue:

This is a health crisis, not specifically an economic one. It could certainly head that way if the economy remains closed for too long, but at present, it simply isn’t.

The economy was humming along just fine before COVID-19 hit. Remember how everyone was predicting a recession in 2018, in response to the trade war?

It never happened. Instead, productivity soared. Unemployment hit record lows.

The March retail and manufacturing statistics, while worse than analyst estimates, should not be surprising in the slightest. The U.S. is, after all, in uncharted territory.

Anything can and will happen. As a result, attempting to gauge the precise economic impact of COVID-19 ahead of time is a fool’s errand. The market already knows things are going to look bad for quite a while.

What truly matters is its response to a recovery. Or, at the very least, the belief that a recovery is coming.

If President Trump says tomorrow that he’s ready to open the economy back up on May 1st, stocks will soar. Poor quarterly earnings and economic data will fall by the wayside as bulls retake control. If he extends the lockdown to June, look out below.

The COVID-19 pandemic rattled the U.S. economy. There’s no doubt about it. I can guarantee you that April’s retail and manufacturing numbers will look terrible, too.

But, thankfully, none of that will matter if the U.S. snaps back by Q3. And with new coronavirus cases on the decline, it seems as though we’re headed in that direction.

Regardless of how disappointed analysts may currently be.

{kind=link}