Covid-19 infections are surging across the U.S., Trump’s legal team says they have enough evidence to overturn the election results, and Treasury Secretary Steven Mnuchin just pulled the plug on several Federal Reserve lending programs.

Still, stocks have managed to stay afloat. All three major indexes are trading relatively flat as of noon.

And it’s not just a vaccine that has bulls keeping the faith. Wall Street’s confidence is providing a massive bullish influence as well.

That’s something the hedge funds would never admit to, though. Several weeks ago, JPMorgan fund managers said that, overall, the big investment groups remain mostly on the sidelines.

But according to a report from Goldman Sachs, that appears to be completely false. Instead, hedge funds have grown historically bullish, to the point at which they’ve never been longer on stocks, on both a gross and net basis.

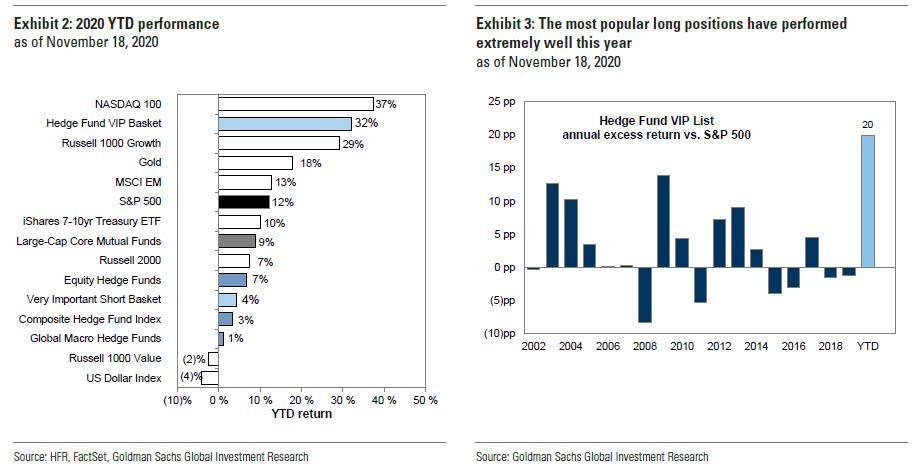

It’s all spelled out in a hedge fund trend monitor from Goldman’s Ben Snider, who says hedge funds “increasingly relied on beta to support returns” in the third quarter. The most popular hedge fund long positions (as tracked by Goldman’s Hedge Fund VIP Basket in the chart below) have outperformed the S&P 500 by 20%, posting a year-to-date (YTD) return of 32% vs. the S&P’s 12%.

The hedge funds haven’t beat the Nasdaq Composite YTD, but when compared to the S&P, they’re on track to post their best results since Goldman began measuring the positions.

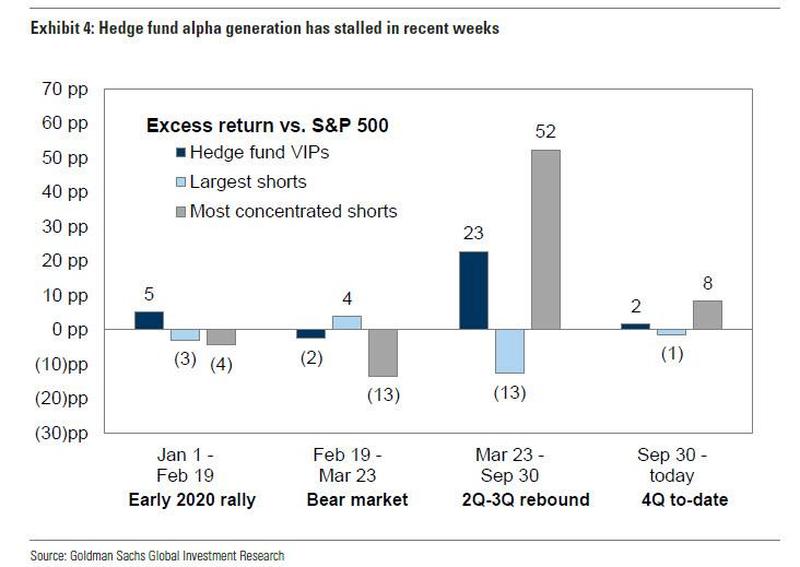

Even better than those long trades, though, were Q3 shorts, which posted the biggest gains of the quarter.

“Since the market trough in March the most concentrated short positions have consistently outperformed as funds covered their short exposures in a rapidly rising market.”

Now (Q4), however, outstanding short positions have cratered. Hedge funds are buying back-in after several highly effective Covid-19 vaccines were announced.

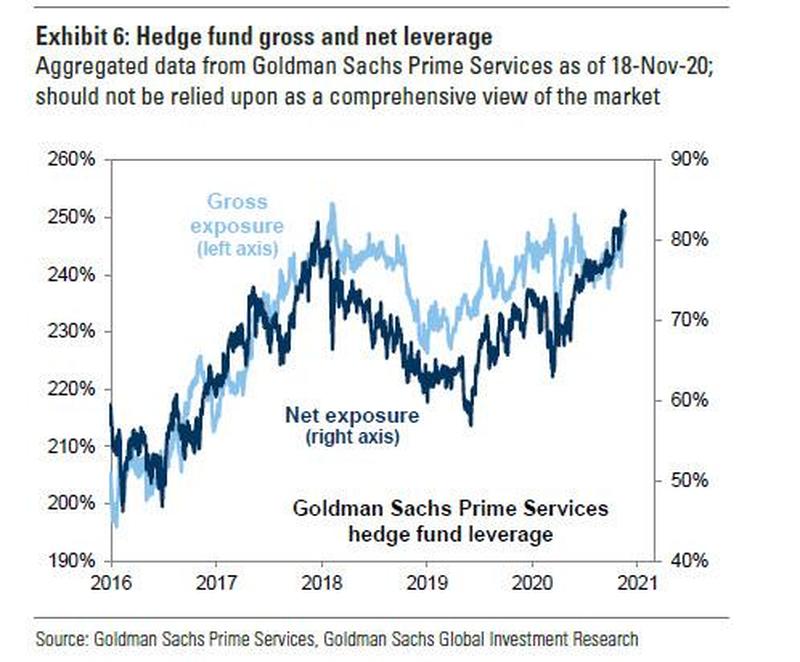

But the most damning evidence of a bullish swoon came from Goldman’s chart measuring hedge fund leverage:

“According to [this] data, net leverage has risen quickly since the March market trough and is now at the highest level on record,” Snider explained.

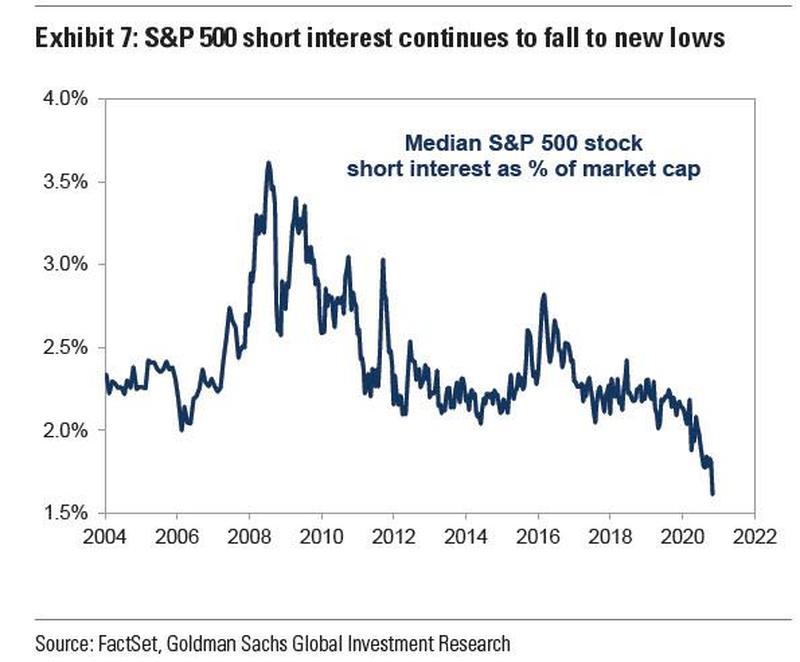

Meanwhile, Goldman observed a sharp decline in S&P 500 short interest as it fell to its lowest level ever measured in the chart’s 16-year history:

Snider added in his report that “short interest has continued to fall, reaching new record lows.”

So, in other words, hedge funds are stacking leverage like never before while S&P shorts plummet in both total interest as well as the outstanding number of VIP shorts.

Earlier in the week, we shared key pieces of Bank of America’s November Fund Managers Survey that more or less confirmed Snider’s findings. In BofA’s report, it was clear that fund manager sentiment was highly bullish across the board.

That spooked BofA’s strategists enough to recommend selling in a follow-up note to clients.

And if you look at how the market’s top stocks have traded this week, it’s apparent that the vaccine rally is beginning to lose steam.

If stocks “round the corner” any further, they’ll find themselves in reversal territory, prompting an abrupt shift in strategy from hedge funds.

Keep in mind, that doesn’t necessarily mean a major correction is coming. Or that the market’s long-term prospects have soured.

But it should serve as a strong indicator of how fragile the current rally is, and, more importantly, how bulls could be in for some short-term pain.

Until equities truly start to drop, though, playing along with Wall Street – and staying long on stocks – remains the best course of action.

Just be prepared to sell when the “chicken littles” of the market get too scared and start “clucking” in unison.

{kind=link}