Is the Fed going to hike into a grim recession? That’s what investors were asking themselves this morning after more confounding economic data rolled in. Despite slumping retail sales and warnings from banks of an impending recession, the jobs market still looks strong on the surface according to new unemployment numbers.

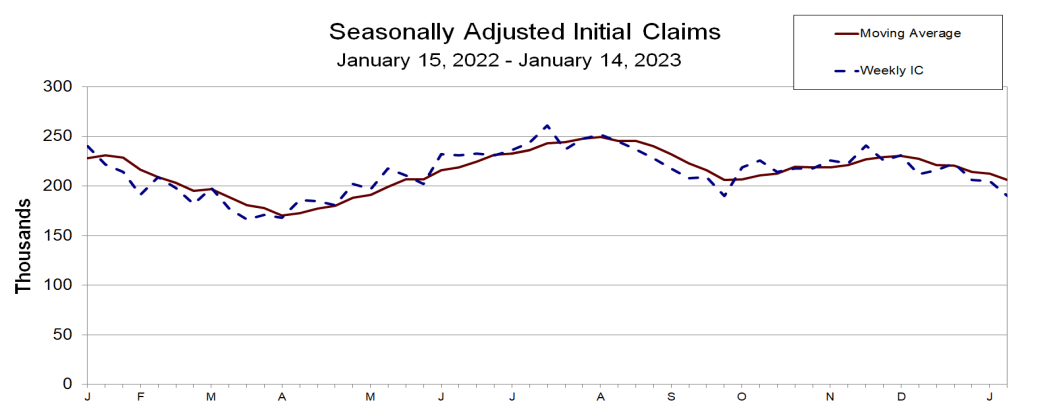

Initial weekly jobless claims for last week were released this morning, revealing a new low unseen since last September. That’s not what bulls wanted to see.

“Despite all the big-tech post-pandemic layoffs, the jobs market remains hot,” said Oanda analyst Ed Moya.

“The labor market needs to break to allow the Fed to comfortably keep rates on hold.”

For US labor, good news is still considered bad news. But is bad news also bad news now with an economic slowdown seemingly on the horizon?

It’s an idea we floated last year; because of the unique scenario the Fed is currently facing:

Tight labor, high inflation, and a recession.

Virtually all news (outside of falling inflation or a soft jobs report) could be received as bearish these days as a result.

Yesterday’s poor retail sales data, which would have been seen as bullish at any other time over the last two years, was interpreted as a warning of a “hard landing.” Stocks sank after the report was released.

And though the S&P’s selloff was likely driven by technical factors – most notably, a failure to breach the 200-day moving average and its major bearish trendline – weak retail sales certainly didn’t help.

Wall Street has increasingly gotten on board with this concept in recent weeks.

“Yesterday’s soft growth data (Retail Sales, Industrial Production, NY Fed Biz Activity) drove a reversal in index gains that had seen buyers early in the session following the weaker than expected PPI print,” wrote JPMorgan’s head of market intelligence, Andrew Tyler.

“While the PPI data gives additional evidence that the disinflation narrative is the correct one, this may have given way to fears on growth and expectations the US has a hard landing. Is this most recent rally over? It appears so.”

Tyler concluded:

“While US Market Intelligence began the year neutral-to-bullish, it is beginning to feel like we are entering a ‘bad news is bad news’ market as the disinflation narrative has become consensus.”

Not everyone agrees that the “disinflation narrative” is the one to follow, though. JPMorgan CEO Jamie Dimon appeared on CNBC today to remind investors that inflation remains a problem for the Fed, and to not be complacent on rates.

“I actually think rates are probably going to go higher than 5 percent […] because I think there’s a lot of underlying inflation, which won’t go away so quick,” Dimon said.

He specifically pointed to falling energy prices and slowed growth in China, which both served to limit inflation in recent months. These disinflationary pressures were merely temporary and could become major drivers of inflation in the future, Dimon explained.

He then went on to say that the fed funds rate may even need to rise to 6 percent.

Morgan Stanley CEO James Gorman disagreed with Dimon’s take, saying that he thinks a hike to 6% would be “surprising.” Gorman sees the Fed pausing its hikes after another two 25 basis point increases.

“I’ve been in a happy land of four, four, and four — roughly 4 percent unemployment, 4 percent inflation, 4 percent rates,” Gorman quipped.

“Rates will be a little higher. Employment at this stage is a little lower, and inflation has been higher. But if we get in that kind of zone, we can deal with it. That would be an appropriate time to pause.”

That’s certainly a bullish outlook given the base case of 5% rates.

Regardless of who’s right, it seems as though bulls – not the Fed – are ready to pause. Another move lower tomorrow for the S&P would, in all likelihood, confirm a deeper short-term retracement as the market adheres to its longer-term downtrend.

{kind=link}